Dear Friends and Partners,

In the first half of 2021, the Flexible Fixed Income Fund returned +6.3%. Since the Fund’s inception in early 2016, it has delivered a compound annual return of +7.4%.

2021 has been a period of differentiation for the fund. Despite having low net exposure relative to its history, the Fund has produced returns meaningfully in excess of its benchmarks. This is owing to our continued application of the Fund’s flexible investment strategy, owning a narrow collection of favorable ideas across the credit spectrum. With the exception of glaring sector-wide pricing distortions, which we take periodic advantage of, we continue to be focused on opportunities at the micro-level. Individual opportunities and portfolio composition may vary in security type - secured, unsecured, convertible, preferred – but our focus on risk adjusted returns remains the same.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF.

2021: A Year of Many Firsts

To say that 2021 is an unusual year is like saying that Warren Buffett or Mark Leonard is an above average investor (a massive understatement, to be clear). This year has been host to a wide variety of phenomena that make this part of the cycle as exciting and entertaining as they are foreboding:

Former US Treasury Secretary Larry Summers remarked this month:

"We're driving our car at 100 miles an hour on a road that is empty right now but won't always be empty and I don't know what form the accident will come, but when you're driving 100 miles an hour it's probably not actually the fastest way to get where you're going because you're likely to have some kind of dislocation."

As the Federal Reserve begins to consider winding down its record stimulus programs, this perspective lands quite well. In the meantime, we continue to marvel at a situation where monetary and fiscal stimulus have combined to fuel a spectacular inflation of nearly all financial assets. “Stimmy checks” sent to many Americans have contributed to a replay reminiscent of the dot-com bubble, where retail investors are back to being a prominent feature of the market, causing massive distortions in certain areas of markets. What is different this time around is that social media has proven to be a potent accelerant, encouraging "YOLO" (you only live once) and "FOMO" (fear of missing out) behaviour in many assets including:

"Meme investments" such as Gamestop and Dogecoin. Gamestop equity saw a 17-fold increase in the month of January. Dogecoin, a cryptocurrency that was originally made as a joke, saw a 52-fold year-to-date rally by May to reach a peak aggregate market value of 89 billion dollars.1

Bitcoin. The apparent posterchild of the Bitcoin craze is Michael Saylor. Saylor is the CEO of a multibillion dollar publicly traded, software-turned-bitcoin-holding company and in June told investors “once you know how it all ends, the only use of time is, ‘How do I buy more Bitcoin?’ Take all your money, buy Bitcoin…. and if you absolutely love the thing that you don't want to sell, go mortgage your house and buy bitcoin with it and if you've got a business that you love because your family works for the business, it's in your family for 37 years and you can't bear to sell it, mortgage it and convert the proceeds into the hardest money on earth which is bitcoin.”

Finally, we are seeing other things like a single-location deli in New Jersey that generated only fourteen thousand dollars in sales in 2020 that somehow saw a two billion dollar valuation. For those looking to get rich quick by merging a frozen banana stand into a SPAC, this has been the year to do it.

High Expectations

All of these anecdotes bring to life just how untethered from reality securities prices can get. By many measures, equity and credit markets are pricing in the smoothest of future conditions. The economy will grow. The Federal Reserve will deftly taper and normalize interest rates. Inflation will moderate. Geopolitical conflicts will cool. These are the types of assumptions that seem embedded in the market consensus, for now.

Just as Jeff Bezos has remarked “the stock is not the company and the company is not the stock”, the same can be said about the economy and financial markets. It is intuitive that the performance of these two entities should have a relatively tight relationship, but this isn’t always the case. History demonstrates that even when we have seen excellent economic growth, it is actually far from certain that financial markets will closely match these outcomes. It would probably strike most people as impossible that we could see a flat stock market amidst an economic expansion of 300%2, but that is precisely what happened in the United States from early 1966 to late 1982. This fact of history bears repeating. Over a period lasting nearly 17 years, the Dow Jones Industrial Average Index (DJIA) saw essentially no gain in price while the economy expanded by approximately 320 percent. If we adjust both indices similarly for inflation3 the result is equally staggering: the DJIA declined by 66 percent in real terms while the economy expanded by 54%4. In retrospect, it was not particularly surprising to see in 1977 Warren Buffett write in Fortune explaining to the investing public “How Inflation Swindles the Equity Investor.” The economy is not the market indeed.

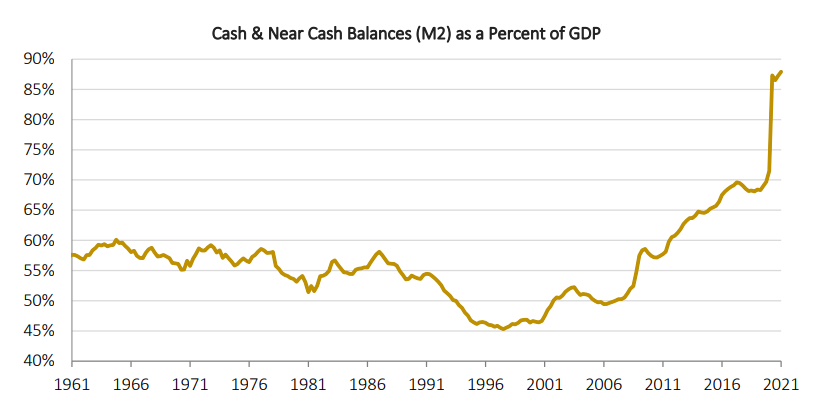

Admittedly, yields on ten-year US Treasury bonds increased by 5 percentage points over this period. However, looking at today’s situation, with the ten-year treasury at 1.4%, core inflation currently running at 4.5%, onshoring of global supply chains, all-time high cash levels in the economy and what seems like somewhat open-ended monetary and fiscal stimulus, it does not strike us that higher long term interest rates and inflation should be dismissed as a possibility, particularly due to the punishing consequences of being wrong.

Parts of the stock market are not the only place there exists of a consensus of a flawless future. In investment grade bonds, the additional expected yield that an owner receives over a risk-free government bond (also known as the “credit spread”) is near all time lows. In the high yield market, we have all time low levels of yield, at a paltry 3.7%5. Dipping down in credit quality does not solve the dilemma, as CCC-rated bonds, at a meagre 5.5%6, yield a full percentage point less than they have at anytime in their history prior to 2020.

The Good News is That Attractive Investments Do Still Exist

From a top-down perspective, investment risk appears high. But from a bottom-up perspective, there are still solid investments to be found. It just takes turning over more rocks. We have found select Canadian high yield and listed debt issuers continue to have good risk-reward relationships and we have assembled a collection of relatively short duration high yield bonds that we believe offer between three and five percent return expectations. Issuers such as Parkland Corporation (gas stations), Superior Plus (propane delivery) and Kruger Products (tissue and packaging) are good examples of the defensive, dependable credits we own. These issuers, along with other defensive investments comprise more than 50% of the portfolio and form the core of our below-average exposure to the credit market. Given the solid credit profile of these issuers and the relatively low duration of this segment of the portfolio, we believe these investments will hold up very well, rain or shine.

We also are seeing plenty of corporate actions, which bring with them a variety of attractive prospective investment opportunities. Our recently realized investment in the Shaw Communications Preferred Shares serves as a good example that outsized returns are achievable if one is at the ready to expend focused time to research and efficiently execute the right prospective investment. Further, our opportunistic investment in the convertible bonds of J2 Global in the summer of 2020 continues to bear fruit as the company announced strong earnings and a spinoff transaction which has been exceedingly well-received by equity investors (through which our convertible benefits). Given current wide-open credit conditions and prospective changes to capital gains taxes, we expect corporate activity to heat up and opportunity sets to expand as we proceed through the year.

The Silver Lining of Market Exuberance

Sometimes, certain sector valuations simply go too far. While it is easy to complain about the extreme complacency seen in the credit market, it’s better to do something about it. Today we see a wonderful opportunity to hedge against negative market surprises through the investment grade bond space.

Valuation Risk

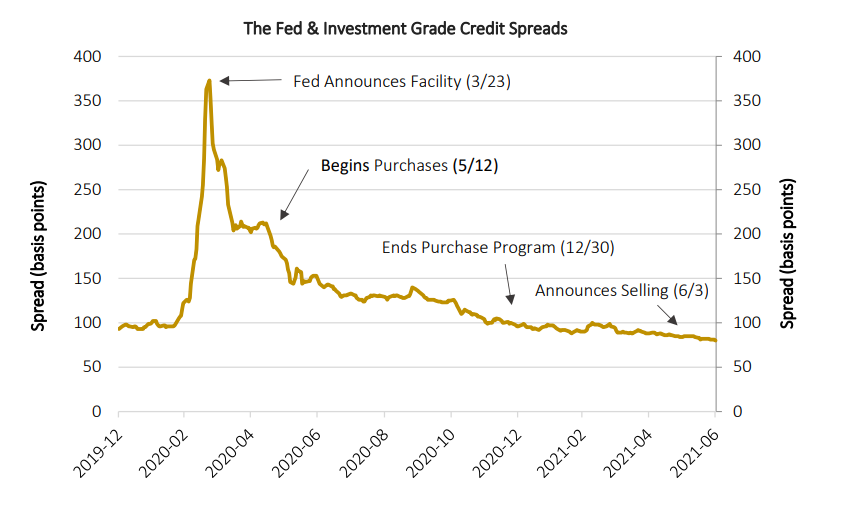

Right now, we think the investment grade credit market contains an incredibly optimistic consensus, perhaps stronger than we’ve ever seen before. Pricing is at a level that appears to reflect a valuation overshoot, with the market coasting to ever more expensive levels merely on what we would attribute to the narrative artifact of “the Fed's got our back” that saturated the psyches of investors over the last year and a half. It is worth unpacking what has happened over this time to truly understand that this “Fed Put” should be thought of as irrelevant at current valuations.

Looking back to the second and third weeks of March 2020, by most appearances one could have concluded there was a run underway on corporate bond markets. And, to solve this issue, one could have presumed that the Federal Reserve really needed to be in the market immediately. As it turns out, the Fed’s mere commitment that it would buy corporate bonds under a large purchase programme was sufficient to turn the market tide. By the time the Fed got its ducks in a row to actually purchase bonds in the market in May of 2020, the market had already rocketed out of its pit of despair. The market move(down and up) was entirely driven by psychology. We find this a remarkable lesson and is a prime demonstration of how fickle markets can be. The Fed Put in investment grade bonds was left effectivelyuntested10 and by the end of 2020, the Fed quietly ended purchases under its facility. Finally, by June2021, in an apparent response to very frothy market conditions, the Fed actually made a surprise announcement of unwinding the facility. Based on the fact that the Fed is a seller of corporate securities, it would be a stretch to expect the Fed Put to return to the corporate market anytime before the next crisis, In the absence of this technical support, valuation risk in the investment grade market is clearly high.

Fundamental Risk

Current fundamental risk in investment grade is also at the highest level ever seen in history. From a credit perspective, the share of BBB rated debt has expanded from 20% to more than 50% over the last20 years. Interest rate risk has increased by more than 50% as well over this same time period with duration expanding from 5.5 to 8.25 years. Based on current balance sheets (leverage/credit risk) and security attributes (interest rate risk), the market has more risk in it than ever. Prospective fundamental risk is high and increasing as well. What do you get when you combine near record-low costs of debt, record high stock market valuations, an expanding economy and CEO confidence at the highest levels since 1983? Our bet is on stock buybacks and debt-fueled M&A activity. These activities are detrimental to creditors.

The Risk-to-Reward Proposition

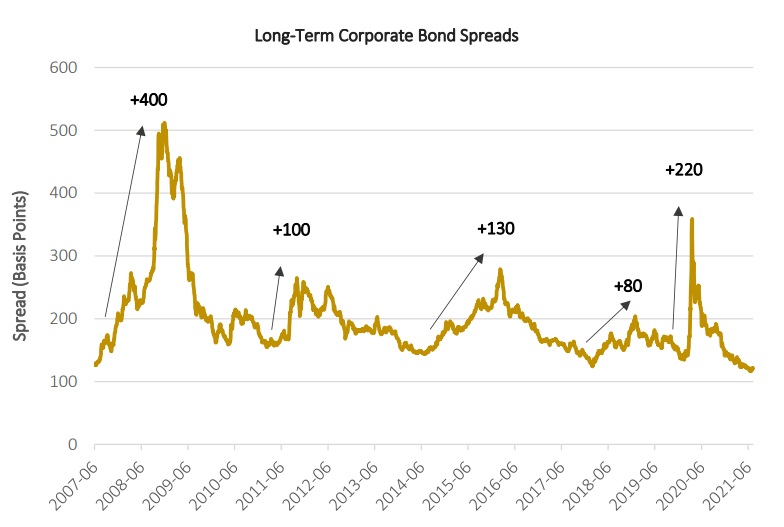

Following the Great Financial Crisis, we have seen four instances of material credit market weakness, as measured by increases in credit spreads.

During these periods of credit spread widening, corporate bonds fall in price relative to government bonds. This effect is magnified particularly in long-term (30-40 year) corporate bonds. Excluding the Great Financial Crisis, in the long-term corporate bond sector we have seen credit spread widening of anywhere from 0.8% to 2.2% during these periods of weakness. Due to the fact that long-term bond prices are exceptionally sensitive to changes in credit spreads combined with credit spreads being at multi-decade lows, investment risk appears to be at peak levels in this space. If spreads widen, watch out.

What the Bond Math Tells Us

Let’s take Verizon Communications’ 3% Notes due 2060 for example. This bond has a yield that is 1.25% higher than its like-maturity US Treasury bond. If this 1.25% spread increases by one percentage point to a 2.25% spread, it results in a price decline of 19% in the Verizon long bond. Given we’ve seen increases of more than 1% in long corporate bond spreads on three occasions in the last ten years, it could be argued that a widening of more than one percentage point from current levels is a very reasonable potential outcome.

The Reward-to-Risk in Numbers

When we compare the potential payoff of 19%, we can see how attractive this payoff structure is in the context of its carrying cost. Shorting Verizon’s bond versus owning a similar maturity Treasury bond has a potential payoff of 19% relative to a very modest 1.25% carrying cost (plus modest borrow fees). This investment offers an approximate 15:1 relationship of potential return versus its annual carrying cost. This highly favorable payoff structure also means the position doesn’t require great market timing, since the carrying costs are so low. Finally, if there were to be a more significant seizure in financial markets like we saw in early 2020, where credit spreads widened by more than 2%, this payoff would improve to34%, a payoff that nearly equals the drawdown seen in the stock market at the time. All this for a mid 1%carrying cost strikes us as a once-in-a-cycle opportunity that is currently presenting itself. This risk/reward relationship reminds us of George Soros’ oft-noted comment which is “it's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.” We like the 15:1 payoff on something that has happened (for some reason or another)three times in the last ten years.

Why This Opportunity is Available

So, if this is such a no-brainer, what’s in it for the buyers of these long corporate bonds? In the words of a bulge bracket institutional credit salesperson “nobody is in the long end unless they have to be.” In addition to the Federal Reserve pushing many investors out the risk curve, most long-term investment grade bond buyers are “LDI” (liability driven investment) managers who are focused on managing long dated obligations. These buyers are less concerned with absolute levels of compensation as they are with simply matching cash inflows with outflows far in the future. Asian institutions, specifically, are a major player in this sector of the market and their buying (or selling) is driven typically by how much additional yield they can earn after hedging costs. Right now, a yield advantage exists and hedging costs are very low, but this is likely to change as the Federal Reserve raises interest rates. Suffice it to say that the utility of these bonds are not evergreen in the eyes of this large market constituent.

The Nuts and Bolts of it

A meaningful allocation to investments that benefit from widening long-term corporate bond spreads isn’t particularly commonplace in asset management. To express this view, large funds would have to diversify across hundreds of bonds in order to avoid too much issue concentration risk. This vastly shrinks the number of funds able to execute on this opportunity. In addition, the notion of paying out premium for an indefinite amount of time in exchange for an uncertain (but hopefully outsized) gain is not particularly compatible with the very nature of many investors, particularly those in fixed income. Many investors would prefer to make money 85% of the time regardless of the consequences of the other 15% of the time. This lumpiness in the return profile is a contributing factor in why this type of investment is undervalued in the first place.

Déjà Vu in the Ewing Morris Fixed Income Department

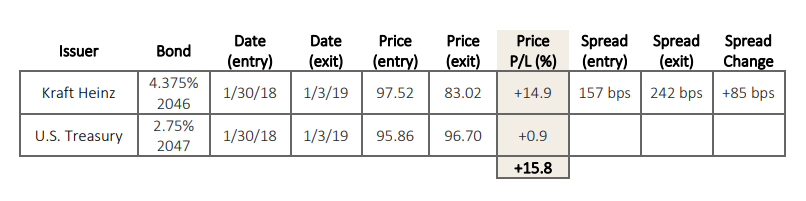

It should be noted that we’ve executed on this investment before. In early 2018 we identified an excellent backdrop in the consumer packaged food space to take advantage of a similar setup. The investment thesis was communicated in our 2017 annual letter, reviewed in our 2018 performance report card and was later noted in Bloomberg. Below is portfolio activity from a sample bond from this basket. Kraft Heinz credit spreads widened by 0.85% from their all-time tights, which produced a 16%price profit from the short position versus a long US Treasury. Subtracting a years’ worth of carry (spread+ borrow cost) from the investment resulted in a total return of about 14% for the position. Today we are pleased to see this opportunity available across the entire sector.

Our Perspective on Today’s Market

Markets tend to be uncomfortable places at times of unusual levels of valuation, but they don’t have to be. As the investments we have made contain a comfortable gap between price and value and our hedges have been well-set, we are moving forward with confidence in a market that should warrant plenty of caution.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

1Coinmarketcap.com

2US Nominal GDP - Federal Reserve Economic Database (FRED)

3Using the GDP Implicit Price Deflator - FRED - Series: USAGDPDEFQISMEI

4Bloomberg, FRED

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged)and iShares Canadian Corporate Bond Index ETF as benchmark indices as these are widely known and usedbenchmark indices for fixed income markets. The Fund has a flexible investment mandate and thus these benchmarkindices are provided for information only. Comparisons to benchmarks and indices have limitations. The Fund doesnot invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fundportfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source: CapitalIQ, Bloomberg and Ewing Morris. As of June 30, 2021.

Dear Friends and Partners,

In the first half of 2021, the Flexible Fixed Income Fund returned +6.3%. Since the Fund’s inception in early 2016, it has delivered a compound annual return of +7.4%.

2021 has been a period of differentiation for the fund. Despite having low net exposure relative to its history, the Fund has produced returns meaningfully in excess of its benchmarks. This is owing to our continued application of the Fund’s flexible investment strategy, owning a narrow collection of favorable ideas across the credit spectrum. With the exception of glaring sector-wide pricing distortions, which we take periodic advantage of, we continue to be focused on opportunities at the micro-level. Individual opportunities and portfolio composition may vary in security type - secured, unsecured, convertible, preferred – but our focus on risk adjusted returns remains the same.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF.

2021: A Year of Many Firsts

To say that 2021 is an unusual year is like saying that Warren Buffett or Mark Leonard is an above average investor (a massive understatement, to be clear). This year has been host to a wide variety of phenomena that make this part of the cycle as exciting and entertaining as they are foreboding:

Former US Treasury Secretary Larry Summers remarked this month:

"We're driving our car at 100 miles an hour on a road that is empty right now but won't always be empty and I don't know what form the accident will come, but when you're driving 100 miles an hour it's probably not actually the fastest way to get where you're going because you're likely to have some kind of dislocation."

As the Federal Reserve begins to consider winding down its record stimulus programs, this perspective lands quite well. In the meantime, we continue to marvel at a situation where monetary and fiscal stimulus have combined to fuel a spectacular inflation of nearly all financial assets. “Stimmy checks” sent to many Americans have contributed to a replay reminiscent of the dot-com bubble, where retail investors are back to being a prominent feature of the market, causing massive distortions in certain areas of markets. What is different this time around is that social media has proven to be a potent accelerant, encouraging "YOLO" (you only live once) and "FOMO" (fear of missing out) behaviour in many assets including:

"Meme investments" such as Gamestop and Dogecoin. Gamestop equity saw a 17-fold increase in the month of January. Dogecoin, a cryptocurrency that was originally made as a joke, saw a 52-fold year-to-date rally by May to reach a peak aggregate market value of 89 billion dollars.1

Bitcoin. The apparent posterchild of the Bitcoin craze is Michael Saylor. Saylor is the CEO of a multibillion dollar publicly traded, software-turned-bitcoin-holding company and in June told investors “once you know how it all ends, the only use of time is, ‘How do I buy more Bitcoin?’ Take all your money, buy Bitcoin…. and if you absolutely love the thing that you don't want to sell, go mortgage your house and buy bitcoin with it and if you've got a business that you love because your family works for the business, it's in your family for 37 years and you can't bear to sell it, mortgage it and convert the proceeds into the hardest money on earth which is bitcoin.”

Finally, we are seeing other things like a single-location deli in New Jersey that generated only fourteen thousand dollars in sales in 2020 that somehow saw a two billion dollar valuation. For those looking to get rich quick by merging a frozen banana stand into a SPAC, this has been the year to do it.

High Expectations

All of these anecdotes bring to life just how untethered from reality securities prices can get. By many measures, equity and credit markets are pricing in the smoothest of future conditions. The economy will grow. The Federal Reserve will deftly taper and normalize interest rates. Inflation will moderate. Geopolitical conflicts will cool. These are the types of assumptions that seem embedded in the market consensus, for now.

Just as Jeff Bezos has remarked “the stock is not the company and the company is not the stock”, the same can be said about the economy and financial markets. It is intuitive that the performance of these two entities should have a relatively tight relationship, but this isn’t always the case. History demonstrates that even when we have seen excellent economic growth, it is actually far from certain that financial markets will closely match these outcomes. It would probably strike most people as impossible that we could see a flat stock market amidst an economic expansion of 300%2, but that is precisely what happened in the United States from early 1966 to late 1982. This fact of history bears repeating. Over a period lasting nearly 17 years, the Dow Jones Industrial Average Index (DJIA) saw essentially no gain in price while the economy expanded by approximately 320 percent. If we adjust both indices similarly for inflation3 the result is equally staggering: the DJIA declined by 66 percent in real terms while the economy expanded by 54%4. In retrospect, it was not particularly surprising to see in 1977 Warren Buffett write in Fortune explaining to the investing public “How Inflation Swindles the Equity Investor.” The economy is not the market indeed.

Admittedly, yields on ten-year US Treasury bonds increased by 5 percentage points over this period. However, looking at today’s situation, with the ten-year treasury at 1.4%, core inflation currently running at 4.5%, onshoring of global supply chains, all-time high cash levels in the economy and what seems like somewhat open-ended monetary and fiscal stimulus, it does not strike us that higher long term interest rates and inflation should be dismissed as a possibility, particularly due to the punishing consequences of being wrong.

Parts of the stock market are not the only place there exists of a consensus of a flawless future. In investment grade bonds, the additional expected yield that an owner receives over a risk-free government bond (also known as the “credit spread”) is near all time lows. In the high yield market, we have all time low levels of yield, at a paltry 3.7%5. Dipping down in credit quality does not solve the dilemma, as CCC-rated bonds, at a meagre 5.5%6, yield a full percentage point less than they have at anytime in their history prior to 2020.

The Good News is That Attractive Investments Do Still Exist

From a top-down perspective, investment risk appears high. But from a bottom-up perspective, there are still solid investments to be found. It just takes turning over more rocks. We have found select Canadian high yield and listed debt issuers continue to have good risk-reward relationships and we have assembled a collection of relatively short duration high yield bonds that we believe offer between three and five percent return expectations. Issuers such as Parkland Corporation (gas stations), Superior Plus (propane delivery) and Kruger Products (tissue and packaging) are good examples of the defensive, dependable credits we own. These issuers, along with other defensive investments comprise more than 50% of the portfolio and form the core of our below-average exposure to the credit market. Given the solid credit profile of these issuers and the relatively low duration of this segment of the portfolio, we believe these investments will hold up very well, rain or shine.

We also are seeing plenty of corporate actions, which bring with them a variety of attractive prospective investment opportunities. Our recently realized investment in the Shaw Communications Preferred Shares serves as a good example that outsized returns are achievable if one is at the ready to expend focused time to research and efficiently execute the right prospective investment. Further, our opportunistic investment in the convertible bonds of J2 Global in the summer of 2020 continues to bear fruit as the company announced strong earnings and a spinoff transaction which has been exceedingly well-received by equity investors (through which our convertible benefits). Given current wide-open credit conditions and prospective changes to capital gains taxes, we expect corporate activity to heat up and opportunity sets to expand as we proceed through the year.

The Silver Lining of Market Exuberance

Sometimes, certain sector valuations simply go too far. While it is easy to complain about the extreme complacency seen in the credit market, it’s better to do something about it. Today we see a wonderful opportunity to hedge against negative market surprises through the investment grade bond space.

Valuation Risk

Right now, we think the investment grade credit market contains an incredibly optimistic consensus, perhaps stronger than we’ve ever seen before. Pricing is at a level that appears to reflect a valuation overshoot, with the market coasting to ever more expensive levels merely on what we would attribute to the narrative artifact of “the Fed's got our back” that saturated the psyches of investors over the last year and a half. It is worth unpacking what has happened over this time to truly understand that this “Fed Put” should be thought of as irrelevant at current valuations.

Looking back to the second and third weeks of March 2020, by most appearances one could have concluded there was a run underway on corporate bond markets. And, to solve this issue, one could have presumed that the Federal Reserve really needed to be in the market immediately. As it turns out, the Fed’s mere commitment that it would buy corporate bonds under a large purchase programme was sufficient to turn the market tide. By the time the Fed got its ducks in a row to actually purchase bonds in the market in May of 2020, the market had already rocketed out of its pit of despair. The market move(down and up) was entirely driven by psychology. We find this a remarkable lesson and is a prime demonstration of how fickle markets can be. The Fed Put in investment grade bonds was left effectivelyuntested10 and by the end of 2020, the Fed quietly ended purchases under its facility. Finally, by June2021, in an apparent response to very frothy market conditions, the Fed actually made a surprise announcement of unwinding the facility. Based on the fact that the Fed is a seller of corporate securities, it would be a stretch to expect the Fed Put to return to the corporate market anytime before the next crisis, In the absence of this technical support, valuation risk in the investment grade market is clearly high.

Fundamental Risk

Current fundamental risk in investment grade is also at the highest level ever seen in history. From a credit perspective, the share of BBB rated debt has expanded from 20% to more than 50% over the last20 years. Interest rate risk has increased by more than 50% as well over this same time period with duration expanding from 5.5 to 8.25 years. Based on current balance sheets (leverage/credit risk) and security attributes (interest rate risk), the market has more risk in it than ever. Prospective fundamental risk is high and increasing as well. What do you get when you combine near record-low costs of debt, record high stock market valuations, an expanding economy and CEO confidence at the highest levels since 1983? Our bet is on stock buybacks and debt-fueled M&A activity. These activities are detrimental to creditors.

The Risk-to-Reward Proposition

Following the Great Financial Crisis, we have seen four instances of material credit market weakness, as measured by increases in credit spreads.

During these periods of credit spread widening, corporate bonds fall in price relative to government bonds. This effect is magnified particularly in long-term (30-40 year) corporate bonds. Excluding the Great Financial Crisis, in the long-term corporate bond sector we have seen credit spread widening of anywhere from 0.8% to 2.2% during these periods of weakness. Due to the fact that long-term bond prices are exceptionally sensitive to changes in credit spreads combined with credit spreads being at multi-decade lows, investment risk appears to be at peak levels in this space. If spreads widen, watch out.

What the Bond Math Tells Us

Let’s take Verizon Communications’ 3% Notes due 2060 for example. This bond has a yield that is 1.25% higher than its like-maturity US Treasury bond. If this 1.25% spread increases by one percentage point to a 2.25% spread, it results in a price decline of 19% in the Verizon long bond. Given we’ve seen increases of more than 1% in long corporate bond spreads on three occasions in the last ten years, it could be argued that a widening of more than one percentage point from current levels is a very reasonable potential outcome.

The Reward-to-Risk in Numbers

When we compare the potential payoff of 19%, we can see how attractive this payoff structure is in the context of its carrying cost. Shorting Verizon’s bond versus owning a similar maturity Treasury bond has a potential payoff of 19% relative to a very modest 1.25% carrying cost (plus modest borrow fees). This investment offers an approximate 15:1 relationship of potential return versus its annual carrying cost. This highly favorable payoff structure also means the position doesn’t require great market timing, since the carrying costs are so low. Finally, if there were to be a more significant seizure in financial markets like we saw in early 2020, where credit spreads widened by more than 2%, this payoff would improve to34%, a payoff that nearly equals the drawdown seen in the stock market at the time. All this for a mid 1%carrying cost strikes us as a once-in-a-cycle opportunity that is currently presenting itself. This risk/reward relationship reminds us of George Soros’ oft-noted comment which is “it's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.” We like the 15:1 payoff on something that has happened (for some reason or another)three times in the last ten years.

Why This Opportunity is Available

So, if this is such a no-brainer, what’s in it for the buyers of these long corporate bonds? In the words of a bulge bracket institutional credit salesperson “nobody is in the long end unless they have to be.” In addition to the Federal Reserve pushing many investors out the risk curve, most long-term investment grade bond buyers are “LDI” (liability driven investment) managers who are focused on managing long dated obligations. These buyers are less concerned with absolute levels of compensation as they are with simply matching cash inflows with outflows far in the future. Asian institutions, specifically, are a major player in this sector of the market and their buying (or selling) is driven typically by how much additional yield they can earn after hedging costs. Right now, a yield advantage exists and hedging costs are very low, but this is likely to change as the Federal Reserve raises interest rates. Suffice it to say that the utility of these bonds are not evergreen in the eyes of this large market constituent.

The Nuts and Bolts of it

A meaningful allocation to investments that benefit from widening long-term corporate bond spreads isn’t particularly commonplace in asset management. To express this view, large funds would have to diversify across hundreds of bonds in order to avoid too much issue concentration risk. This vastly shrinks the number of funds able to execute on this opportunity. In addition, the notion of paying out premium for an indefinite amount of time in exchange for an uncertain (but hopefully outsized) gain is not particularly compatible with the very nature of many investors, particularly those in fixed income. Many investors would prefer to make money 85% of the time regardless of the consequences of the other 15% of the time. This lumpiness in the return profile is a contributing factor in why this type of investment is undervalued in the first place.

Déjà Vu in the Ewing Morris Fixed Income Department

It should be noted that we’ve executed on this investment before. In early 2018 we identified an excellent backdrop in the consumer packaged food space to take advantage of a similar setup. The investment thesis was communicated in our 2017 annual letter, reviewed in our 2018 performance report card and was later noted in Bloomberg. Below is portfolio activity from a sample bond from this basket. Kraft Heinz credit spreads widened by 0.85% from their all-time tights, which produced a 16%price profit from the short position versus a long US Treasury. Subtracting a years’ worth of carry (spread+ borrow cost) from the investment resulted in a total return of about 14% for the position. Today we are pleased to see this opportunity available across the entire sector.

Our Perspective on Today’s Market

Markets tend to be uncomfortable places at times of unusual levels of valuation, but they don’t have to be. As the investments we have made contain a comfortable gap between price and value and our hedges have been well-set, we are moving forward with confidence in a market that should warrant plenty of caution.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

1Coinmarketcap.com

2US Nominal GDP - Federal Reserve Economic Database (FRED)

3Using the GDP Implicit Price Deflator - FRED - Series: USAGDPDEFQISMEI

4Bloomberg, FRED

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged)and iShares Canadian Corporate Bond Index ETF as benchmark indices as these are widely known and usedbenchmark indices for fixed income markets. The Fund has a flexible investment mandate and thus these benchmarkindices are provided for information only. Comparisons to benchmarks and indices have limitations. The Fund doesnot invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fundportfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source: CapitalIQ, Bloomberg and Ewing Morris. As of June 30, 2021.

Dear Friends and Partners,

In the first half of 2021, the Flexible Fixed Income Fund returned +6.3%. Since the Fund’s inception in early 2016, it has delivered a compound annual return of +7.4%.

2021 has been a period of differentiation for the fund. Despite having low net exposure relative to its history, the Fund has produced returns meaningfully in excess of its benchmarks. This is owing to our continued application of the Fund’s flexible investment strategy, owning a narrow collection of favorable ideas across the credit spectrum. With the exception of glaring sector-wide pricing distortions, which we take periodic advantage of, we continue to be focused on opportunities at the micro-level. Individual opportunities and portfolio composition may vary in security type - secured, unsecured, convertible, preferred – but our focus on risk adjusted returns remains the same.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF.

2021: A Year of Many Firsts

To say that 2021 is an unusual year is like saying that Warren Buffett or Mark Leonard is an above average investor (a massive understatement, to be clear). This year has been host to a wide variety of phenomena that make this part of the cycle as exciting and entertaining as they are foreboding:

Former US Treasury Secretary Larry Summers remarked this month:

"We're driving our car at 100 miles an hour on a road that is empty right now but won't always be empty and I don't know what form the accident will come, but when you're driving 100 miles an hour it's probably not actually the fastest way to get where you're going because you're likely to have some kind of dislocation."

As the Federal Reserve begins to consider winding down its record stimulus programs, this perspective lands quite well. In the meantime, we continue to marvel at a situation where monetary and fiscal stimulus have combined to fuel a spectacular inflation of nearly all financial assets. “Stimmy checks” sent to many Americans have contributed to a replay reminiscent of the dot-com bubble, where retail investors are back to being a prominent feature of the market, causing massive distortions in certain areas of markets. What is different this time around is that social media has proven to be a potent accelerant, encouraging "YOLO" (you only live once) and "FOMO" (fear of missing out) behaviour in many assets including:

"Meme investments" such as Gamestop and Dogecoin. Gamestop equity saw a 17-fold increase in the month of January. Dogecoin, a cryptocurrency that was originally made as a joke, saw a 52-fold year-to-date rally by May to reach a peak aggregate market value of 89 billion dollars.1

Bitcoin. The apparent posterchild of the Bitcoin craze is Michael Saylor. Saylor is the CEO of a multibillion dollar publicly traded, software-turned-bitcoin-holding company and in June told investors “once you know how it all ends, the only use of time is, ‘How do I buy more Bitcoin?’ Take all your money, buy Bitcoin…. and if you absolutely love the thing that you don't want to sell, go mortgage your house and buy bitcoin with it and if you've got a business that you love because your family works for the business, it's in your family for 37 years and you can't bear to sell it, mortgage it and convert the proceeds into the hardest money on earth which is bitcoin.”

Finally, we are seeing other things like a single-location deli in New Jersey that generated only fourteen thousand dollars in sales in 2020 that somehow saw a two billion dollar valuation. For those looking to get rich quick by merging a frozen banana stand into a SPAC, this has been the year to do it.

High Expectations

All of these anecdotes bring to life just how untethered from reality securities prices can get. By many measures, equity and credit markets are pricing in the smoothest of future conditions. The economy will grow. The Federal Reserve will deftly taper and normalize interest rates. Inflation will moderate. Geopolitical conflicts will cool. These are the types of assumptions that seem embedded in the market consensus, for now.

Just as Jeff Bezos has remarked “the stock is not the company and the company is not the stock”, the same can be said about the economy and financial markets. It is intuitive that the performance of these two entities should have a relatively tight relationship, but this isn’t always the case. History demonstrates that even when we have seen excellent economic growth, it is actually far from certain that financial markets will closely match these outcomes. It would probably strike most people as impossible that we could see a flat stock market amidst an economic expansion of 300%2, but that is precisely what happened in the United States from early 1966 to late 1982. This fact of history bears repeating. Over a period lasting nearly 17 years, the Dow Jones Industrial Average Index (DJIA) saw essentially no gain in price while the economy expanded by approximately 320 percent. If we adjust both indices similarly for inflation3 the result is equally staggering: the DJIA declined by 66 percent in real terms while the economy expanded by 54%4. In retrospect, it was not particularly surprising to see in 1977 Warren Buffett write in Fortune explaining to the investing public “How Inflation Swindles the Equity Investor.” The economy is not the market indeed.

Admittedly, yields on ten-year US Treasury bonds increased by 5 percentage points over this period. However, looking at today’s situation, with the ten-year treasury at 1.4%, core inflation currently running at 4.5%, onshoring of global supply chains, all-time high cash levels in the economy and what seems like somewhat open-ended monetary and fiscal stimulus, it does not strike us that higher long term interest rates and inflation should be dismissed as a possibility, particularly due to the punishing consequences of being wrong.

Parts of the stock market are not the only place there exists of a consensus of a flawless future. In investment grade bonds, the additional expected yield that an owner receives over a risk-free government bond (also known as the “credit spread”) is near all time lows. In the high yield market, we have all time low levels of yield, at a paltry 3.7%5. Dipping down in credit quality does not solve the dilemma, as CCC-rated bonds, at a meagre 5.5%6, yield a full percentage point less than they have at anytime in their history prior to 2020.

The Good News is That Attractive Investments Do Still Exist

From a top-down perspective, investment risk appears high. But from a bottom-up perspective, there are still solid investments to be found. It just takes turning over more rocks. We have found select Canadian high yield and listed debt issuers continue to have good risk-reward relationships and we have assembled a collection of relatively short duration high yield bonds that we believe offer between three and five percent return expectations. Issuers such as Parkland Corporation (gas stations), Superior Plus (propane delivery) and Kruger Products (tissue and packaging) are good examples of the defensive, dependable credits we own. These issuers, along with other defensive investments comprise more than 50% of the portfolio and form the core of our below-average exposure to the credit market. Given the solid credit profile of these issuers and the relatively low duration of this segment of the portfolio, we believe these investments will hold up very well, rain or shine.

We also are seeing plenty of corporate actions, which bring with them a variety of attractive prospective investment opportunities. Our recently realized investment in the Shaw Communications Preferred Shares serves as a good example that outsized returns are achievable if one is at the ready to expend focused time to research and efficiently execute the right prospective investment. Further, our opportunistic investment in the convertible bonds of J2 Global in the summer of 2020 continues to bear fruit as the company announced strong earnings and a spinoff transaction which has been exceedingly well-received by equity investors (through which our convertible benefits). Given current wide-open credit conditions and prospective changes to capital gains taxes, we expect corporate activity to heat up and opportunity sets to expand as we proceed through the year.

The Silver Lining of Market Exuberance

Sometimes, certain sector valuations simply go too far. While it is easy to complain about the extreme complacency seen in the credit market, it’s better to do something about it. Today we see a wonderful opportunity to hedge against negative market surprises through the investment grade bond space.

Valuation Risk

Right now, we think the investment grade credit market contains an incredibly optimistic consensus, perhaps stronger than we’ve ever seen before. Pricing is at a level that appears to reflect a valuation overshoot, with the market coasting to ever more expensive levels merely on what we would attribute to the narrative artifact of “the Fed's got our back” that saturated the psyches of investors over the last year and a half. It is worth unpacking what has happened over this time to truly understand that this “Fed Put” should be thought of as irrelevant at current valuations.

Looking back to the second and third weeks of March 2020, by most appearances one could have concluded there was a run underway on corporate bond markets. And, to solve this issue, one could have presumed that the Federal Reserve really needed to be in the market immediately. As it turns out, the Fed’s mere commitment that it would buy corporate bonds under a large purchase programme was sufficient to turn the market tide. By the time the Fed got its ducks in a row to actually purchase bonds in the market in May of 2020, the market had already rocketed out of its pit of despair. The market move(down and up) was entirely driven by psychology. We find this a remarkable lesson and is a prime demonstration of how fickle markets can be. The Fed Put in investment grade bonds was left effectivelyuntested10 and by the end of 2020, the Fed quietly ended purchases under its facility. Finally, by June2021, in an apparent response to very frothy market conditions, the Fed actually made a surprise announcement of unwinding the facility. Based on the fact that the Fed is a seller of corporate securities, it would be a stretch to expect the Fed Put to return to the corporate market anytime before the next crisis, In the absence of this technical support, valuation risk in the investment grade market is clearly high.

Fundamental Risk

Current fundamental risk in investment grade is also at the highest level ever seen in history. From a credit perspective, the share of BBB rated debt has expanded from 20% to more than 50% over the last20 years. Interest rate risk has increased by more than 50% as well over this same time period with duration expanding from 5.5 to 8.25 years. Based on current balance sheets (leverage/credit risk) and security attributes (interest rate risk), the market has more risk in it than ever. Prospective fundamental risk is high and increasing as well. What do you get when you combine near record-low costs of debt, record high stock market valuations, an expanding economy and CEO confidence at the highest levels since 1983? Our bet is on stock buybacks and debt-fueled M&A activity. These activities are detrimental to creditors.

The Risk-to-Reward Proposition

Following the Great Financial Crisis, we have seen four instances of material credit market weakness, as measured by increases in credit spreads.

During these periods of credit spread widening, corporate bonds fall in price relative to government bonds. This effect is magnified particularly in long-term (30-40 year) corporate bonds. Excluding the Great Financial Crisis, in the long-term corporate bond sector we have seen credit spread widening of anywhere from 0.8% to 2.2% during these periods of weakness. Due to the fact that long-term bond prices are exceptionally sensitive to changes in credit spreads combined with credit spreads being at multi-decade lows, investment risk appears to be at peak levels in this space. If spreads widen, watch out.

What the Bond Math Tells Us

Let’s take Verizon Communications’ 3% Notes due 2060 for example. This bond has a yield that is 1.25% higher than its like-maturity US Treasury bond. If this 1.25% spread increases by one percentage point to a 2.25% spread, it results in a price decline of 19% in the Verizon long bond. Given we’ve seen increases of more than 1% in long corporate bond spreads on three occasions in the last ten years, it could be argued that a widening of more than one percentage point from current levels is a very reasonable potential outcome.

The Reward-to-Risk in Numbers

When we compare the potential payoff of 19%, we can see how attractive this payoff structure is in the context of its carrying cost. Shorting Verizon’s bond versus owning a similar maturity Treasury bond has a potential payoff of 19% relative to a very modest 1.25% carrying cost (plus modest borrow fees). This investment offers an approximate 15:1 relationship of potential return versus its annual carrying cost. This highly favorable payoff structure also means the position doesn’t require great market timing, since the carrying costs are so low. Finally, if there were to be a more significant seizure in financial markets like we saw in early 2020, where credit spreads widened by more than 2%, this payoff would improve to34%, a payoff that nearly equals the drawdown seen in the stock market at the time. All this for a mid 1%carrying cost strikes us as a once-in-a-cycle opportunity that is currently presenting itself. This risk/reward relationship reminds us of George Soros’ oft-noted comment which is “it's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.” We like the 15:1 payoff on something that has happened (for some reason or another)three times in the last ten years.

Why This Opportunity is Available

So, if this is such a no-brainer, what’s in it for the buyers of these long corporate bonds? In the words of a bulge bracket institutional credit salesperson “nobody is in the long end unless they have to be.” In addition to the Federal Reserve pushing many investors out the risk curve, most long-term investment grade bond buyers are “LDI” (liability driven investment) managers who are focused on managing long dated obligations. These buyers are less concerned with absolute levels of compensation as they are with simply matching cash inflows with outflows far in the future. Asian institutions, specifically, are a major player in this sector of the market and their buying (or selling) is driven typically by how much additional yield they can earn after hedging costs. Right now, a yield advantage exists and hedging costs are very low, but this is likely to change as the Federal Reserve raises interest rates. Suffice it to say that the utility of these bonds are not evergreen in the eyes of this large market constituent.

The Nuts and Bolts of it

A meaningful allocation to investments that benefit from widening long-term corporate bond spreads isn’t particularly commonplace in asset management. To express this view, large funds would have to diversify across hundreds of bonds in order to avoid too much issue concentration risk. This vastly shrinks the number of funds able to execute on this opportunity. In addition, the notion of paying out premium for an indefinite amount of time in exchange for an uncertain (but hopefully outsized) gain is not particularly compatible with the very nature of many investors, particularly those in fixed income. Many investors would prefer to make money 85% of the time regardless of the consequences of the other 15% of the time. This lumpiness in the return profile is a contributing factor in why this type of investment is undervalued in the first place.

Déjà Vu in the Ewing Morris Fixed Income Department

It should be noted that we’ve executed on this investment before. In early 2018 we identified an excellent backdrop in the consumer packaged food space to take advantage of a similar setup. The investment thesis was communicated in our 2017 annual letter, reviewed in our 2018 performance report card and was later noted in Bloomberg. Below is portfolio activity from a sample bond from this basket. Kraft Heinz credit spreads widened by 0.85% from their all-time tights, which produced a 16%price profit from the short position versus a long US Treasury. Subtracting a years’ worth of carry (spread+ borrow cost) from the investment resulted in a total return of about 14% for the position. Today we are pleased to see this opportunity available across the entire sector.

Our Perspective on Today’s Market

Markets tend to be uncomfortable places at times of unusual levels of valuation, but they don’t have to be. As the investments we have made contain a comfortable gap between price and value and our hedges have been well-set, we are moving forward with confidence in a market that should warrant plenty of caution.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

1Coinmarketcap.com

2US Nominal GDP - Federal Reserve Economic Database (FRED)

3Using the GDP Implicit Price Deflator - FRED - Series: USAGDPDEFQISMEI

4Bloomberg, FRED

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged)and iShares Canadian Corporate Bond Index ETF as benchmark indices as these are widely known and usedbenchmark indices for fixed income markets. The Fund has a flexible investment mandate and thus these benchmarkindices are provided for information only. Comparisons to benchmarks and indices have limitations. The Fund doesnot invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fundportfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source: CapitalIQ, Bloomberg and Ewing Morris. As of June 30, 2021.

Dear Friends and Partners,

In the first half of 2021, the Flexible Fixed Income Fund returned +6.3%. Since the Fund’s inception in early 2016, it has delivered a compound annual return of +7.4%.

2021 has been a period of differentiation for the fund. Despite having low net exposure relative to its history, the Fund has produced returns meaningfully in excess of its benchmarks. This is owing to our continued application of the Fund’s flexible investment strategy, owning a narrow collection of favorable ideas across the credit spectrum. With the exception of glaring sector-wide pricing distortions, which we take periodic advantage of, we continue to be focused on opportunities at the micro-level. Individual opportunities and portfolio composition may vary in security type - secured, unsecured, convertible, preferred – but our focus on risk adjusted returns remains the same.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF.

2021: A Year of Many Firsts

To say that 2021 is an unusual year is like saying that Warren Buffett or Mark Leonard is an above average investor (a massive understatement, to be clear). This year has been host to a wide variety of phenomena that make this part of the cycle as exciting and entertaining as they are foreboding:

Former US Treasury Secretary Larry Summers remarked this month:

"We're driving our car at 100 miles an hour on a road that is empty right now but won't always be empty and I don't know what form the accident will come, but when you're driving 100 miles an hour it's probably not actually the fastest way to get where you're going because you're likely to have some kind of dislocation."

As the Federal Reserve begins to consider winding down its record stimulus programs, this perspective lands quite well. In the meantime, we continue to marvel at a situation where monetary and fiscal stimulus have combined to fuel a spectacular inflation of nearly all financial assets. “Stimmy checks” sent to many Americans have contributed to a replay reminiscent of the dot-com bubble, where retail investors are back to being a prominent feature of the market, causing massive distortions in certain areas of markets. What is different this time around is that social media has proven to be a potent accelerant, encouraging "YOLO" (you only live once) and "FOMO" (fear of missing out) behaviour in many assets including:

"Meme investments" such as Gamestop and Dogecoin. Gamestop equity saw a 17-fold increase in the month of January. Dogecoin, a cryptocurrency that was originally made as a joke, saw a 52-fold year-to-date rally by May to reach a peak aggregate market value of 89 billion dollars.1

Bitcoin. The apparent posterchild of the Bitcoin craze is Michael Saylor. Saylor is the CEO of a multibillion dollar publicly traded, software-turned-bitcoin-holding company and in June told investors “once you know how it all ends, the only use of time is, ‘How do I buy more Bitcoin?’ Take all your money, buy Bitcoin…. and if you absolutely love the thing that you don't want to sell, go mortgage your house and buy bitcoin with it and if you've got a business that you love because your family works for the business, it's in your family for 37 years and you can't bear to sell it, mortgage it and convert the proceeds into the hardest money on earth which is bitcoin.”

Finally, we are seeing other things like a single-location deli in New Jersey that generated only fourteen thousand dollars in sales in 2020 that somehow saw a two billion dollar valuation. For those looking to get rich quick by merging a frozen banana stand into a SPAC, this has been the year to do it.

High Expectations

All of these anecdotes bring to life just how untethered from reality securities prices can get. By many measures, equity and credit markets are pricing in the smoothest of future conditions. The economy will grow. The Federal Reserve will deftly taper and normalize interest rates. Inflation will moderate. Geopolitical conflicts will cool. These are the types of assumptions that seem embedded in the market consensus, for now.

Just as Jeff Bezos has remarked “the stock is not the company and the company is not the stock”, the same can be said about the economy and financial markets. It is intuitive that the performance of these two entities should have a relatively tight relationship, but this isn’t always the case. History demonstrates that even when we have seen excellent economic growth, it is actually far from certain that financial markets will closely match these outcomes. It would probably strike most people as impossible that we could see a flat stock market amidst an economic expansion of 300%2, but that is precisely what happened in the United States from early 1966 to late 1982. This fact of history bears repeating. Over a period lasting nearly 17 years, the Dow Jones Industrial Average Index (DJIA) saw essentially no gain in price while the economy expanded by approximately 320 percent. If we adjust both indices similarly for inflation3 the result is equally staggering: the DJIA declined by 66 percent in real terms while the economy expanded by 54%4. In retrospect, it was not particularly surprising to see in 1977 Warren Buffett write in Fortune explaining to the investing public “How Inflation Swindles the Equity Investor.” The economy is not the market indeed.

Admittedly, yields on ten-year US Treasury bonds increased by 5 percentage points over this period. However, looking at today’s situation, with the ten-year treasury at 1.4%, core inflation currently running at 4.5%, onshoring of global supply chains, all-time high cash levels in the economy and what seems like somewhat open-ended monetary and fiscal stimulus, it does not strike us that higher long term interest rates and inflation should be dismissed as a possibility, particularly due to the punishing consequences of being wrong.

Parts of the stock market are not the only place there exists of a consensus of a flawless future. In investment grade bonds, the additional expected yield that an owner receives over a risk-free government bond (also known as the “credit spread”) is near all time lows. In the high yield market, we have all time low levels of yield, at a paltry 3.7%5. Dipping down in credit quality does not solve the dilemma, as CCC-rated bonds, at a meagre 5.5%6, yield a full percentage point less than they have at anytime in their history prior to 2020.

The Good News is That Attractive Investments Do Still Exist

From a top-down perspective, investment risk appears high. But from a bottom-up perspective, there are still solid investments to be found. It just takes turning over more rocks. We have found select Canadian high yield and listed debt issuers continue to have good risk-reward relationships and we have assembled a collection of relatively short duration high yield bonds that we believe offer between three and five percent return expectations. Issuers such as Parkland Corporation (gas stations), Superior Plus (propane delivery) and Kruger Products (tissue and packaging) are good examples of the defensive, dependable credits we own. These issuers, along with other defensive investments comprise more than 50% of the portfolio and form the core of our below-average exposure to the credit market. Given the solid credit profile of these issuers and the relatively low duration of this segment of the portfolio, we believe these investments will hold up very well, rain or shine.

We also are seeing plenty of corporate actions, which bring with them a variety of attractive prospective investment opportunities. Our recently realized investment in the Shaw Communications Preferred Shares serves as a good example that outsized returns are achievable if one is at the ready to expend focused time to research and efficiently execute the right prospective investment. Further, our opportunistic investment in the convertible bonds of J2 Global in the summer of 2020 continues to bear fruit as the company announced strong earnings and a spinoff transaction which has been exceedingly well-received by equity investors (through which our convertible benefits). Given current wide-open credit conditions and prospective changes to capital gains taxes, we expect corporate activity to heat up and opportunity sets to expand as we proceed through the year.

The Silver Lining of Market Exuberance

Sometimes, certain sector valuations simply go too far. While it is easy to complain about the extreme complacency seen in the credit market, it’s better to do something about it. Today we see a wonderful opportunity to hedge against negative market surprises through the investment grade bond space.

Valuation Risk

Right now, we think the investment grade credit market contains an incredibly optimistic consensus, perhaps stronger than we’ve ever seen before. Pricing is at a level that appears to reflect a valuation overshoot, with the market coasting to ever more expensive levels merely on what we would attribute to the narrative artifact of “the Fed's got our back” that saturated the psyches of investors over the last year and a half. It is worth unpacking what has happened over this time to truly understand that this “Fed Put” should be thought of as irrelevant at current valuations.

Looking back to the second and third weeks of March 2020, by most appearances one could have concluded there was a run underway on corporate bond markets. And, to solve this issue, one could have presumed that the Federal Reserve really needed to be in the market immediately. As it turns out, the Fed’s mere commitment that it would buy corporate bonds under a large purchase programme was sufficient to turn the market tide. By the time the Fed got its ducks in a row to actually purchase bonds in the market in May of 2020, the market had already rocketed out of its pit of despair. The market move(down and up) was entirely driven by psychology. We find this a remarkable lesson and is a prime demonstration of how fickle markets can be. The Fed Put in investment grade bonds was left effectivelyuntested10 and by the end of 2020, the Fed quietly ended purchases under its facility. Finally, by June2021, in an apparent response to very frothy market conditions, the Fed actually made a surprise announcement of unwinding the facility. Based on the fact that the Fed is a seller of corporate securities, it would be a stretch to expect the Fed Put to return to the corporate market anytime before the next crisis, In the absence of this technical support, valuation risk in the investment grade market is clearly high.

Fundamental Risk

Current fundamental risk in investment grade is also at the highest level ever seen in history. From a credit perspective, the share of BBB rated debt has expanded from 20% to more than 50% over the last20 years. Interest rate risk has increased by more than 50% as well over this same time period with duration expanding from 5.5 to 8.25 years. Based on current balance sheets (leverage/credit risk) and security attributes (interest rate risk), the market has more risk in it than ever. Prospective fundamental risk is high and increasing as well. What do you get when you combine near record-low costs of debt, record high stock market valuations, an expanding economy and CEO confidence at the highest levels since 1983? Our bet is on stock buybacks and debt-fueled M&A activity. These activities are detrimental to creditors.

The Risk-to-Reward Proposition

Following the Great Financial Crisis, we have seen four instances of material credit market weakness, as measured by increases in credit spreads.

During these periods of credit spread widening, corporate bonds fall in price relative to government bonds. This effect is magnified particularly in long-term (30-40 year) corporate bonds. Excluding the Great Financial Crisis, in the long-term corporate bond sector we have seen credit spread widening of anywhere from 0.8% to 2.2% during these periods of weakness. Due to the fact that long-term bond prices are exceptionally sensitive to changes in credit spreads combined with credit spreads being at multi-decade lows, investment risk appears to be at peak levels in this space. If spreads widen, watch out.

What the Bond Math Tells Us

Let’s take Verizon Communications’ 3% Notes due 2060 for example. This bond has a yield that is 1.25% higher than its like-maturity US Treasury bond. If this 1.25% spread increases by one percentage point to a 2.25% spread, it results in a price decline of 19% in the Verizon long bond. Given we’ve seen increases of more than 1% in long corporate bond spreads on three occasions in the last ten years, it could be argued that a widening of more than one percentage point from current levels is a very reasonable potential outcome.

The Reward-to-Risk in Numbers

When we compare the potential payoff of 19%, we can see how attractive this payoff structure is in the context of its carrying cost. Shorting Verizon’s bond versus owning a similar maturity Treasury bond has a potential payoff of 19% relative to a very modest 1.25% carrying cost (plus modest borrow fees). This investment offers an approximate 15:1 relationship of potential return versus its annual carrying cost. This highly favorable payoff structure also means the position doesn’t require great market timing, since the carrying costs are so low. Finally, if there were to be a more significant seizure in financial markets like we saw in early 2020, where credit spreads widened by more than 2%, this payoff would improve to34%, a payoff that nearly equals the drawdown seen in the stock market at the time. All this for a mid 1%carrying cost strikes us as a once-in-a-cycle opportunity that is currently presenting itself. This risk/reward relationship reminds us of George Soros’ oft-noted comment which is “it's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.” We like the 15:1 payoff on something that has happened (for some reason or another)three times in the last ten years.

Why This Opportunity is Available

So, if this is such a no-brainer, what’s in it for the buyers of these long corporate bonds? In the words of a bulge bracket institutional credit salesperson “nobody is in the long end unless they have to be.” In addition to the Federal Reserve pushing many investors out the risk curve, most long-term investment grade bond buyers are “LDI” (liability driven investment) managers who are focused on managing long dated obligations. These buyers are less concerned with absolute levels of compensation as they are with simply matching cash inflows with outflows far in the future. Asian institutions, specifically, are a major player in this sector of the market and their buying (or selling) is driven typically by how much additional yield they can earn after hedging costs. Right now, a yield advantage exists and hedging costs are very low, but this is likely to change as the Federal Reserve raises interest rates. Suffice it to say that the utility of these bonds are not evergreen in the eyes of this large market constituent.

The Nuts and Bolts of it

A meaningful allocation to investments that benefit from widening long-term corporate bond spreads isn’t particularly commonplace in asset management. To express this view, large funds would have to diversify across hundreds of bonds in order to avoid too much issue concentration risk. This vastly shrinks the number of funds able to execute on this opportunity. In addition, the notion of paying out premium for an indefinite amount of time in exchange for an uncertain (but hopefully outsized) gain is not particularly compatible with the very nature of many investors, particularly those in fixed income. Many investors would prefer to make money 85% of the time regardless of the consequences of the other 15% of the time. This lumpiness in the return profile is a contributing factor in why this type of investment is undervalued in the first place.

Déjà Vu in the Ewing Morris Fixed Income Department

It should be noted that we’ve executed on this investment before. In early 2018 we identified an excellent backdrop in the consumer packaged food space to take advantage of a similar setup. The investment thesis was communicated in our 2017 annual letter, reviewed in our 2018 performance report card and was later noted in Bloomberg. Below is portfolio activity from a sample bond from this basket. Kraft Heinz credit spreads widened by 0.85% from their all-time tights, which produced a 16%price profit from the short position versus a long US Treasury. Subtracting a years’ worth of carry (spread+ borrow cost) from the investment resulted in a total return of about 14% for the position. Today we are pleased to see this opportunity available across the entire sector.

Our Perspective on Today’s Market

Markets tend to be uncomfortable places at times of unusual levels of valuation, but they don’t have to be. As the investments we have made contain a comfortable gap between price and value and our hedges have been well-set, we are moving forward with confidence in a market that should warrant plenty of caution.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

1Coinmarketcap.com

2US Nominal GDP - Federal Reserve Economic Database (FRED)

3Using the GDP Implicit Price Deflator - FRED - Series: USAGDPDEFQISMEI

4Bloomberg, FRED

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged)and iShares Canadian Corporate Bond Index ETF as benchmark indices as these are widely known and usedbenchmark indices for fixed income markets. The Fund has a flexible investment mandate and thus these benchmarkindices are provided for information only. Comparisons to benchmarks and indices have limitations. The Fund doesnot invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fundportfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source: CapitalIQ, Bloomberg and Ewing Morris. As of June 30, 2021.

2021 Annual Letter

To the Limited Partners of the Ewing Morris Flexible Fixed Income Fund:

In 2021, the Flexible Fixed Income Fund Returned 8.3%. Since the Fund’s inception in early 2016, it has delivered a compound annual return of 7.1%.