Dear Limited Partners of the Ewing Morris Flexible Fixed Income Fund,

In the first quarter of 2024, the Flexible Fixed Income Fund Returned +2.3%. This return favorably compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and 0%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.1%, meeting our long-term return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin

Free Options on Valuable Change

This year, corporate executives and investment bankers threw a party. M&A volume was up 70% year-over-year in the first quarter. This dynamic was, and continues to be, a welcome development for the fund.

It is welcome because we hold many discounted bonds where if there is a change in ownership of the issuer, the bonds are required to be paid back in full. For a bond trading at a discount to its principal value, this kind of event can pull years of return forward. It is a best-case scenario for bond investors.

So what does it take to be exposed to such a pleasant outcome?

Finding Riches in Niches

Carefully watching for situations that have potential for change is a good start. Sometimes the only thing preventing a corporate sale is sufficient shareholder and board resolve. It turns out that the mental framework of finding signs of emerging power imbalances can produce strong bond investments.

When shareholders get sufficiently energized and step into their power to make change, big events like a corporate sale or divestiture can happen. When a big event happens, it is natural for a bond contract to be implicated. This is usually a good thing for the owner of the bond. It is good for the owner because the owner typically gets back at least 100 cents on the dollar. In a situation like this, a bond priced at a deep discount is typically the best to own to monetize the event.

To this end, we have been increasingly investing in situations featuring shareholder displeasure. The first quarter was host to big events at some of our ~30 portfolio companies. Let us tell you about a couple of them.

Techtarget

We made our investment in Techtarget’s convertible bonds due in 2026 at a price averaging under 80 cents on the dollar in early 2023. Techtarget is a digital media publisher. The day we bought the bonds, shareholders were upset. The stock was down 15% on the day on account of the company reporting disappointing earnings. And, from its 2021 high, the stock was down 62%.

This displeasure was made evident in June of 2023, when the company disclosed its proxy voting results. Shareholders had voted 20% against its directors (on average) and 35% elected ‘against’ on the company’s say-on-pay advisory vote.

So, Techtarget’s leadership chose to do something. On January 10th, 2024, the company entered into a transaction with Informa PLC. As a consequence of this transformative merger, Techtarget bonds are set to receive 100 cents on the dollar - a 25% gain from the purchase price we had made in the prior year.

Catalent

We made our investment in Catalent’s Senior Unsecured bonds due in 2029 and 2030 at a price averaging less than 79 cents on the dollar in May of 2023. Catalent is a drug manufacturer carrying an enterprise value of more than $10B. The day we bought the company’s bonds, the stock was down 77% from its pandemic highs and was in the midst of operational mishaps, financial pressure and accounting delays. The pain was palpable as the embarrassment. The day prior to our first purchase marked the stock’s post-pandemic low of $31.86.

Given the board’s weak position, the company’s size, reasonable balance sheet, and prior media speculation of interest from Danaher, it was no surprise to us that by August the company counted an activist - Elliott Management in this case - as a new prominent shareholder. The two parties signed a cooperation agreement and four new directors were added to the board.

On February 5th, 2024, Catalent press released an agreement to be purchased by Novo Holdings for $63.50. The transaction appears to implicate our bonds’ covenants and the market expects them to be redeemed above 100 cents on the dollar at close, representing a return of more than 27% from our purchase price.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yieald Bond Index ETF (CAD-Hedged), iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg US Corporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2024

Dear Limited Partners of the Ewing Morris Flexible Fixed Income Fund,

In the first quarter of 2024, the Flexible Fixed Income Fund Returned +2.3%. This return favorably compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and 0%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.1%, meeting our long-term return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin

Free Options on Valuable Change

This year, corporate executives and investment bankers threw a party. M&A volume was up 70% year-over-year in the first quarter. This dynamic was, and continues to be, a welcome development for the fund.

It is welcome because we hold many discounted bonds where if there is a change in ownership of the issuer, the bonds are required to be paid back in full. For a bond trading at a discount to its principal value, this kind of event can pull years of return forward. It is a best-case scenario for bond investors.

So what does it take to be exposed to such a pleasant outcome?

Finding Riches in Niches

Carefully watching for situations that have potential for change is a good start. Sometimes the only thing preventing a corporate sale is sufficient shareholder and board resolve. It turns out that the mental framework of finding signs of emerging power imbalances can produce strong bond investments.

When shareholders get sufficiently energized and step into their power to make change, big events like a corporate sale or divestiture can happen. When a big event happens, it is natural for a bond contract to be implicated. This is usually a good thing for the owner of the bond. It is good for the owner because the owner typically gets back at least 100 cents on the dollar. In a situation like this, a bond priced at a deep discount is typically the best to own to monetize the event.

To this end, we have been increasingly investing in situations featuring shareholder displeasure. The first quarter was host to big events at some of our ~30 portfolio companies. Let us tell you about a couple of them.

Techtarget

We made our investment in Techtarget’s convertible bonds due in 2026 at a price averaging under 80 cents on the dollar in early 2023. Techtarget is a digital media publisher. The day we bought the bonds, shareholders were upset. The stock was down 15% on the day on account of the company reporting disappointing earnings. And, from its 2021 high, the stock was down 62%.

This displeasure was made evident in June of 2023, when the company disclosed its proxy voting results. Shareholders had voted 20% against its directors (on average) and 35% elected ‘against’ on the company’s say-on-pay advisory vote.

So, Techtarget’s leadership chose to do something. On January 10th, 2024, the company entered into a transaction with Informa PLC. As a consequence of this transformative merger, Techtarget bonds are set to receive 100 cents on the dollar - a 25% gain from the purchase price we had made in the prior year.

Catalent

We made our investment in Catalent’s Senior Unsecured bonds due in 2029 and 2030 at a price averaging less than 79 cents on the dollar in May of 2023. Catalent is a drug manufacturer carrying an enterprise value of more than $10B. The day we bought the company’s bonds, the stock was down 77% from its pandemic highs and was in the midst of operational mishaps, financial pressure and accounting delays. The pain was palpable as the embarrassment. The day prior to our first purchase marked the stock’s post-pandemic low of $31.86.

Given the board’s weak position, the company’s size, reasonable balance sheet, and prior media speculation of interest from Danaher, it was no surprise to us that by August the company counted an activist - Elliott Management in this case - as a new prominent shareholder. The two parties signed a cooperation agreement and four new directors were added to the board.

On February 5th, 2024, Catalent press released an agreement to be purchased by Novo Holdings for $63.50. The transaction appears to implicate our bonds’ covenants and the market expects them to be redeemed above 100 cents on the dollar at close, representing a return of more than 27% from our purchase price.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yieald Bond Index ETF (CAD-Hedged), iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg US Corporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2024

Dear Limited Partners of the Ewing Morris Flexible Fixed Income Fund,

In the first quarter of 2024, the Flexible Fixed Income Fund Returned +2.3%. This return favorably compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and 0%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.1%, meeting our long-term return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin

Free Options on Valuable Change

This year, corporate executives and investment bankers threw a party. M&A volume was up 70% year-over-year in the first quarter. This dynamic was, and continues to be, a welcome development for the fund.

It is welcome because we hold many discounted bonds where if there is a change in ownership of the issuer, the bonds are required to be paid back in full. For a bond trading at a discount to its principal value, this kind of event can pull years of return forward. It is a best-case scenario for bond investors.

So what does it take to be exposed to such a pleasant outcome?

Finding Riches in Niches

Carefully watching for situations that have potential for change is a good start. Sometimes the only thing preventing a corporate sale is sufficient shareholder and board resolve. It turns out that the mental framework of finding signs of emerging power imbalances can produce strong bond investments.

When shareholders get sufficiently energized and step into their power to make change, big events like a corporate sale or divestiture can happen. When a big event happens, it is natural for a bond contract to be implicated. This is usually a good thing for the owner of the bond. It is good for the owner because the owner typically gets back at least 100 cents on the dollar. In a situation like this, a bond priced at a deep discount is typically the best to own to monetize the event.

To this end, we have been increasingly investing in situations featuring shareholder displeasure. The first quarter was host to big events at some of our ~30 portfolio companies. Let us tell you about a couple of them.

Techtarget

We made our investment in Techtarget’s convertible bonds due in 2026 at a price averaging under 80 cents on the dollar in early 2023. Techtarget is a digital media publisher. The day we bought the bonds, shareholders were upset. The stock was down 15% on the day on account of the company reporting disappointing earnings. And, from its 2021 high, the stock was down 62%.

This displeasure was made evident in June of 2023, when the company disclosed its proxy voting results. Shareholders had voted 20% against its directors (on average) and 35% elected ‘against’ on the company’s say-on-pay advisory vote.

So, Techtarget’s leadership chose to do something. On January 10th, 2024, the company entered into a transaction with Informa PLC. As a consequence of this transformative merger, Techtarget bonds are set to receive 100 cents on the dollar - a 25% gain from the purchase price we had made in the prior year.

Catalent

We made our investment in Catalent’s Senior Unsecured bonds due in 2029 and 2030 at a price averaging less than 79 cents on the dollar in May of 2023. Catalent is a drug manufacturer carrying an enterprise value of more than $10B. The day we bought the company’s bonds, the stock was down 77% from its pandemic highs and was in the midst of operational mishaps, financial pressure and accounting delays. The pain was palpable as the embarrassment. The day prior to our first purchase marked the stock’s post-pandemic low of $31.86.

Given the board’s weak position, the company’s size, reasonable balance sheet, and prior media speculation of interest from Danaher, it was no surprise to us that by August the company counted an activist - Elliott Management in this case - as a new prominent shareholder. The two parties signed a cooperation agreement and four new directors were added to the board.

On February 5th, 2024, Catalent press released an agreement to be purchased by Novo Holdings for $63.50. The transaction appears to implicate our bonds’ covenants and the market expects them to be redeemed above 100 cents on the dollar at close, representing a return of more than 27% from our purchase price.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yieald Bond Index ETF (CAD-Hedged), iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg US Corporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2024

Dear Limited Partners of the Ewing Morris Flexible Fixed Income Fund,

In the first quarter of 2024, the Flexible Fixed Income Fund Returned +2.3%. This return favorably compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and 0%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.1%, meeting our long-term return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin

Free Options on Valuable Change

This year, corporate executives and investment bankers threw a party. M&A volume was up 70% year-over-year in the first quarter. This dynamic was, and continues to be, a welcome development for the fund.

It is welcome because we hold many discounted bonds where if there is a change in ownership of the issuer, the bonds are required to be paid back in full. For a bond trading at a discount to its principal value, this kind of event can pull years of return forward. It is a best-case scenario for bond investors.

So what does it take to be exposed to such a pleasant outcome?

Finding Riches in Niches

Carefully watching for situations that have potential for change is a good start. Sometimes the only thing preventing a corporate sale is sufficient shareholder and board resolve. It turns out that the mental framework of finding signs of emerging power imbalances can produce strong bond investments.

When shareholders get sufficiently energized and step into their power to make change, big events like a corporate sale or divestiture can happen. When a big event happens, it is natural for a bond contract to be implicated. This is usually a good thing for the owner of the bond. It is good for the owner because the owner typically gets back at least 100 cents on the dollar. In a situation like this, a bond priced at a deep discount is typically the best to own to monetize the event.

To this end, we have been increasingly investing in situations featuring shareholder displeasure. The first quarter was host to big events at some of our ~30 portfolio companies. Let us tell you about a couple of them.

Techtarget

We made our investment in Techtarget’s convertible bonds due in 2026 at a price averaging under 80 cents on the dollar in early 2023. Techtarget is a digital media publisher. The day we bought the bonds, shareholders were upset. The stock was down 15% on the day on account of the company reporting disappointing earnings. And, from its 2021 high, the stock was down 62%.

This displeasure was made evident in June of 2023, when the company disclosed its proxy voting results. Shareholders had voted 20% against its directors (on average) and 35% elected ‘against’ on the company’s say-on-pay advisory vote.

So, Techtarget’s leadership chose to do something. On January 10th, 2024, the company entered into a transaction with Informa PLC. As a consequence of this transformative merger, Techtarget bonds are set to receive 100 cents on the dollar - a 25% gain from the purchase price we had made in the prior year.

Catalent

We made our investment in Catalent’s Senior Unsecured bonds due in 2029 and 2030 at a price averaging less than 79 cents on the dollar in May of 2023. Catalent is a drug manufacturer carrying an enterprise value of more than $10B. The day we bought the company’s bonds, the stock was down 77% from its pandemic highs and was in the midst of operational mishaps, financial pressure and accounting delays. The pain was palpable as the embarrassment. The day prior to our first purchase marked the stock’s post-pandemic low of $31.86.

Given the board’s weak position, the company’s size, reasonable balance sheet, and prior media speculation of interest from Danaher, it was no surprise to us that by August the company counted an activist - Elliott Management in this case - as a new prominent shareholder. The two parties signed a cooperation agreement and four new directors were added to the board.

On February 5th, 2024, Catalent press released an agreement to be purchased by Novo Holdings for $63.50. The transaction appears to implicate our bonds’ covenants and the market expects them to be redeemed above 100 cents on the dollar at close, representing a return of more than 27% from our purchase price.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yieald Bond Index ETF (CAD-Hedged), iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg US Corporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2024

2024 Annual Letter

Fellow Limited Partners of the Ewing Morris Flexible Fixed Income Fund,

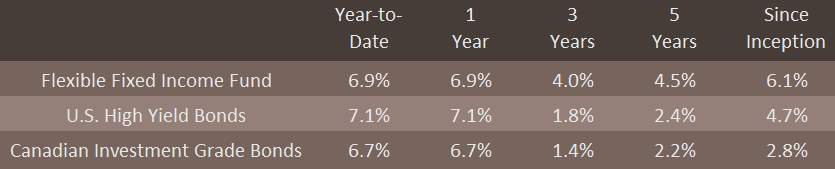

In 2024, the Flexible Fixed Income Fund Returned +6.9%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +7.1% and +6.7%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.1%, meeting our long-term return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

The Year in Review

2024 was an undeniably strong year across many asset classes, especially equities. After being up 25% in2023, the S&P 500 was again up another 24% in 2024. Gold was up 27%. Even the S&P/TSX found itself up 22%.

But fixed income was a different story. Results varied. At a high level, the greater the credit risk taken, the greater the realized reward. This meant more defensive-leaning portfolios lagged.

For example, the (credit) risk-free 10-year US treasury produced total return of -1.7% despite entering the year bearing a 3.9% yield. On the other hand, our high yield benchmark delivered a respectable return in the year of +7.1%.

As for the Flexible Fixed Income Fund - its performance largely kept pace with both our high yield and investment grade benchmarks, providing a +6.9% return. But this result was achieved in spite of a vastly lower credit risk profile throughout the year - not because of it. In 2024, the Fund had two main attributes that made it relatively defensive: lower credit risk investments and equity index hedges.

The lowest quality segment of high yield (CCC rated bonds) was the standout contributor to high yield returns. This part of the market returned 15%. While we don’t avoid these bonds categorically, we simply did not find any bonds in this rating tier attractive enough to own. This may not come as a surprise in light of where we appear to be in the economic cycle and the fact that CCC’s have a 26%default rate.3 By this comparison, we took meaningfully less credit risk than our benchmark. This lower level of risk taking detracted from returns - at least in 2024.

We also saw performance detraction from large cap equity index exposure. As a means to reduce overall risk in the portfolio, we maintained a hedge in the S&P 500, which we unwound in July and September in favor of a hedge with superior upside/downside in investment grade credit. This short exposure detracted 1.2% from returns in the year. We’re also comfortable in concluding that we will be favoring single name equity hedges to credit positions in our portfolio over outright index hedges going forward.

The Opportunity in Investment Grade Credit

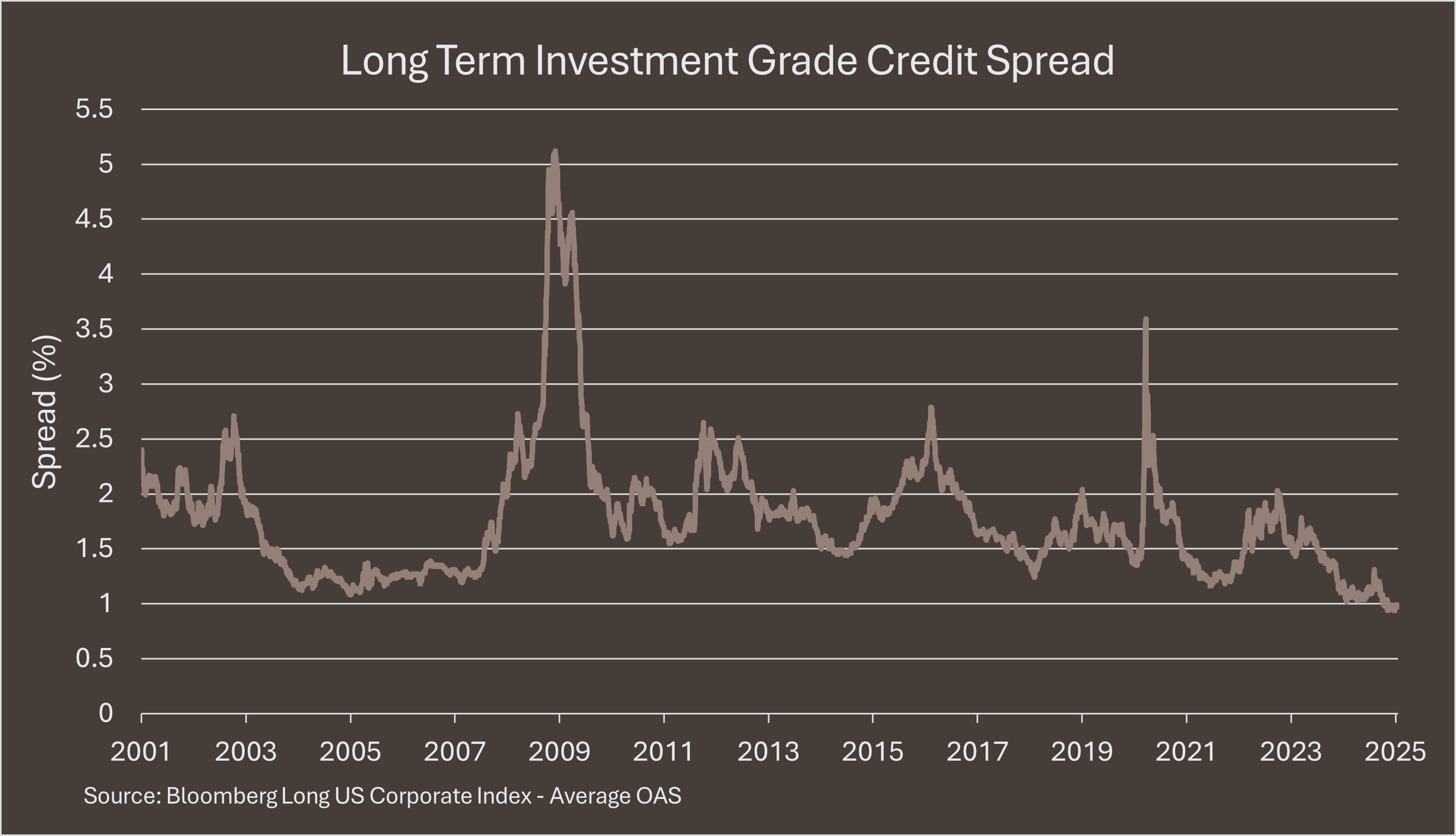

It’s not every day that a fixed income market breaks 24-year records. But, in December this happened in investment grade credit. Compensation for taking credit risk - the extra yield received over the yield of a government bond of a similar term (the ”credit spread”) narrowed to levels we have not seen since the early 2000’s.

History has shown that once credit gets as expensive as it has, investing in a manner that profits from spread widening becomes quite sensible. It’s sensible not only because it offers a large reward relative to its cost, but because it can pay off at a very valuable time: when market conditions are worsening.

What’s attractive to us is that today’s credit spreads carry a kind of certainty about the future: that the economy’s growth trajectory will not change. That G-7 fiscal issues will not be a problem. That the risk of inflation is over. That President Trump will not unsettle the market through his foreign policies or his social media account.

We’ve seen the credit market carry generous assumptions about the future before. In 2021, spreads were exceptionally tight. We took full advantage of this as we outlined in our Q2-2021 Letter and unwound the position profitably in 2022, as we outlined in our Q2-2022 Letter.

At current levels, we believe the opportunity is here again. We have positioned the portfolio through a diversified credit hedge in long term investment grade corporate bonds as a low-cost way to profit from rugged market realities that could easily come into view.

The Deals They Are a Comin’

A logical consequence (and silver lining) of narrow credit spreads is M&A. Regulatory intervention has created a deal-queue of sorts in the past four years. But now, the new administration is likely to turn this queue into a conga line. Almost all other conditions for dealmaking are in place: credit markets are wide open, dry powder at private equity firms is ample and shareholder activism is on the rise. Suffice it to say, the stage is set for a very active year. And we intend to capitalize on it for you.

The Opportunity in Event-Driven Credit

It should come as no surprise that shareholder activism is not a bondholder’s forte. Fortunately, to the great benefit of our fixed income work, we’ve acquired an eye for shareholder engagement thanks to learning from our equity work. This enhanced understanding of corporate governance and shareholder dynamics has resulted in a highly differentiated perspective in fixed income.

With this approach, our job becomes simple (but not easy): first, to find situations where shareholders hold a strong hand in driving for change and second, to find the bonds that benefit the most from this. We are especially interested in this niche because pessimistic credit investors tend to pay nothing for what isn't a matter of fact (or for something that they have not noticed in the first place). Given this dynamic, we believe there exists free option value in certain bonds in the market that fall within this interesting market niche. We have shared examples of this hidden option value in Catalent and Techtarget in our Q1-2024 Letter and we hope to report back with more examples as the year progresses.

Outlook

The forthcoming year appears to be extraordinarily consequential. There exists a wide range of outcomes. We have positioned the portfolio to withstand and capitalize on this array of scenarios. Meanwhile, our process for generating investment ideas has gained in its capacity, supported by careful attention to activist developments and contract-based insight. We are also embracing the newest AI based utilities to enhance the speed of both idea discovery and situational understanding once a high promise prospective investment has been found.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Schedule a

Conversation

Connect with Peers

Explore Our Full Library

Library

Minimizing Tax Drag (Part 2)