To the Limited Partners of the Flexible Fixed Income Fund LP,

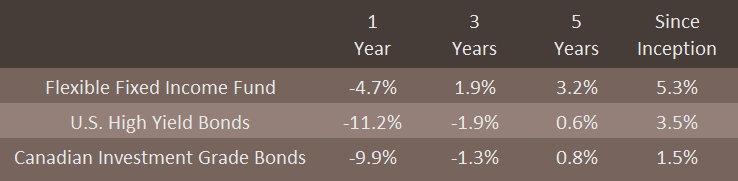

In the second quarter of 2022, the Flexible Fixed Income Fund returned -8.1%. This compares with our high yield and investment grade corporate bond benchmark returns of -9.4% and -5.1%. Since the Fund’s inception in early 2016, the Fund has delivered a compound annual return of +5.1%.

There’s a simple way to frame what has happened in fixed income markets: by May of this year, the bond market had performed worse than any complete year since 1842. While this period hasn’t (yet) been labeled a “crisis,” we are living through one of the most memorable periods that fixed income investors have seen in a generation. Given this backdrop, it is not a surprise that Fund results on an absolute basis are what should ordinarily be viewed as unacceptable. However, widening the aperture only modestly to an 18-month time period reveals the kind of results our approach can deliver. Over this period, we have preserved capital (Fund down 0.7%), while both of our benchmarks (High Yield Bond Index ETF and Canadian Investment Grade Bond Index ETF) are down 10.5% and 13.1%, respectively1. As the history of the Fund has demonstrated, patches of negative returns tend to be temporary and have been followed by strong subsequent performance. For numerous reasons, we believe we are at the front edge of one of the best times to be a high yield bond investor since the inception of the fund more than six years ago.

What's Happened

Before diving into the current state of the market, we’d like to give you an account of how we’ve managed through this historic time. As we expressed in our Q2 2021 letter, we were preparing for the possibility of inflation pressuring the credit market. We shorted the (record expensive) credit risk of long term corporate bonds on the view that inflation (and its consequent central bank tightening) would ultimately impact stock and credit prices. This hedge was executed on a largely diversified basis and was the greatest contributor to our preservation of capital over the last 18 months.

As we moved through 2022, we have been investing increasingly in Structural Value situations. These are investments where the return of the investment is highly specific to the fine print of a bond’s contract. For much of the last thirty years, yields have been falling and bonds have, for the most part, traded above par. When bonds trade above par, the embedded options (like a change of control put right at a price of 101) have no value. However, over the last nine months, a dramatic increase in interest rates has caused a deep decline in bond prices. With bond prices so discounted, events now present a very valuable source of upside - but only if you’ve found the bond contract with the right fine print. This optionality, coupled with plenty of strategic and private equity ‘dry powder,’ presents an underappreciated opportunity set for bond investors in our view. These types of investments have fared far better than the general market as they tend to be shorter-duration and idiosyncratic in nature. For example, in March we purchased Switch Systems 4.125% Sr. Notes due 2029. Less than four months later2, the high yield market is down 7.5%3, while these bonds have generated a return of +3.8%4 owing to the Structural Value embedded in the bond’s contract in connection with a pending takeover of the company by DigitalBridge Group. We have sharpened our focus on situations with this type of setup and have found many of these investments in convertible bonds of technology companies.

The Tax of Inflation Has Entered the Chat

It took a while to happen, but inflation has finally claimed its most obvious victim: the bond market. Returns have been abysmal and finally reflect to a better degree a fair discount rate that incorporates a higher level of expected inflation. Indeed, this period of reappraisal has been a startling process for government bond investors. Furthermore, this volatility in interest rates has caused an increase in the additional yield investors require to own corporate bonds (also known as the “credit spread”). The result of these two factors (increasing rates and credit spreads) is that corporate bond yields are going up (and prices down) even faster than government bonds of the same maturity.

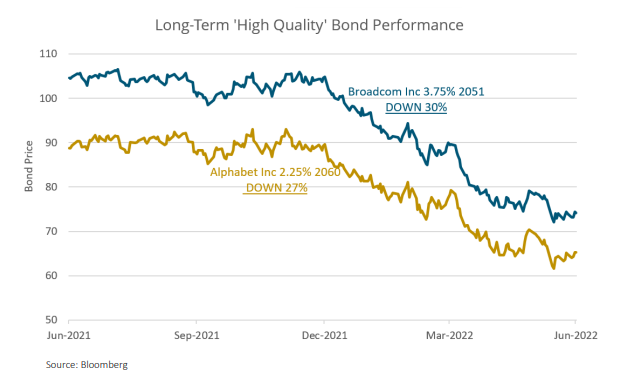

The combination of increasing government bond yields and increasing credit spreads has had an astonishing impact on long-duration corporate bonds. In the span of half a year, many long-term bonds have fallen by 25-35%. Many would be surprised to know that as of this writing, bonds in Google (a company with $134B in cash and only $28B in debt5) are trading at 66 cents6 on the dollar. What’s more is that we do not even own this bond as we are seeing even better opportunities in the market than this.

Opportunities are Nigh

At this juncture, bonds in just about every facet of the corporate bond market have promise and we will highlight three areas: high yield, investment grade and convertible bonds.

High yield is a good place to illuminate first, with expected yields close to their post-great financial crisis highs. In mid-2021, the high yield market once was at 3.5% in yield. Today it sports a desirable yield that has been closing in on 9%.

We are also frequently finding opportunities in investment grade bonds, where contractual features combined with fundamental changes can produce some surprisingly attractive outcomes, relative to the low credit risk of the investment. A good example of this is shorter-term investment grade bonds. These bonds tend to carry exceptionally low credit risk, yet are priced at large discounts (7-10 points) to par, depending on their coupon. On this theme, we own a modest position in Ryder Systems Inc 1.75% Sr. Notes due 2026. Ryder is a transportation and logistics business that has been subject to an informal offer by a private equity firm, which some might see as having put the company ‘in-play’. If a typical take private transaction were to occur at Ryder, under the rules of the bond contract, the bonds would be worth 101. This would represent an overnight gain of 10 points on an event that would not surprise anyone. In the meantime, we are happy to clip our low-risk 4% yield.

Similar Structural Value opportunities are available, in spades, in the convertible bond market. This is because most of the coupons attached to convertible bonds are less than 1%. Most investors buy convertibles for their equity upside. Since the underlying stocks have gone the opposite way intended(down), convertible bonds are now occupying the bargain bin of the corporate bond market. With no equity option value, their economic characteristics have become more like high yield bonds. But, because their coupons are so low, a bond’s “yield” must be earned over time through price appreciation, ultimately culminating at the maturity of the bond, when a bond receives its par payment. A good example of our Structural Value approach as applied in the convertible space is in Everbridge Inc, a company offering critical event communication and asset monitoring technology. Everbridge’s board has found itself to be in a largely indefensible position against a very strong activist campaign which is pushing for a corporate sale. Our principal position in Everbridge is in its 0.125% Sr. Notes due 12/2024. This is a first-to-mature-bond that is covered by cash sitting on Everbridge’s balance sheet. Given the situation, at an 87-dollar price, this investment has a pleasing 15% upside option to par in the event of a corporate sale. In the case this does not happen, we are harvesting a ~6% yield on a cash-covered bond over a two and a half-year term, largely in the tax-efficient form of capital gains.

Admittedly, with the credit market on its back, one should not hold their breath for a take-private deal. However, this still leaves open the likelihood of strategic transactions producing attractive results in a target company’s bonds. Take Resolute Forest Products for example; this freshly announced deal demonstrates that the option value that exists across the entire bond market is real. At an average price of 85 cents, our portfolio is well-positioned for events like this. In fact, we have already have been monetizing these opportunities to date as we discussed in our Q1 2022 letter to Limited Partners.

The Stock Market’s Boss is the Credit Market

The theory goes that if a company cannot service its interest obligations and repay its debt in full at maturity, it's equity value is worthless. Considering high yield bond yields7 moving from 3.5% to 9% (with the market basically closed today) and investment grade bond yields8 moving from 1.75% to 5%, one might want to check whether the stock market’s expected return has become two to three times more attractive in the last 18 months. We make note of this due to the fact that the S&P 500 is down only 20%year-to-date9. We would also point out that this decline followed a 29% climb in 2021 and an 18% climb in the COVID-riddled year of 2020. Given these facts (and equity’s downward-inflecting earnings outlooks) the prices of stocks appear too high if you are as pessimistic as the corporate bond market.

The Path Forward

While we have a highly uncertain economic (and geopolitical) future, there are scores of solid credit investments on sale today in the market. This, more than anything gives us much optimism as we go forward; and this is not just a feeling. Data show that once the market carries a yield of more than 10%, there is an 88% probability of positive returns, 18 months thereafter10. Those are some great odds.

And we’re not the only ones excited. Famed corporate debt investor, Howard Marks, in a recent interview with the Financial Times said that “today I am starting to behave aggressively.” This stood out to us as Marks is quite a conservative investor. The best example of this conservatism was on display in Marks’s April 6, 2020 memo, where he was quite balanced in his outlook (and even held out his expectation for lower asset prices in April). Marks is certainly not a perma-bull.

There are a lot of scenarios under which higher yielding securities work nicely, particularly relative to the broader stock market. We believe the coming quarter will be host to some of the best entry points yet owing to what will be likely a double-threat of downward inflecting results and a negative reset of corporate outlooks. Despite what could be a tough second quarter earnings season, we keep in mind what Marks said in the same interview which was that “the idea of waiting for the bottom is a terrible idea.” On this basis, we are fully invested in securities that, in our opinion, have lower aggregate risk than the high yield market. This allows us the capacity to become more aggressive if even greater bargains reveal themselves. We look forward to taking advantage of what’s to come on your behalf and we thank you for your continued confidence.

***

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures for more details.

118-Month Cumulative Returns as of June 30, 2022.

23/23/2022-7/13/2022

3iShares US High Yield Bond Index Fund (CAD-Hedged)

4Source: Bloomberg

5Source: Company Financials, Bloomberg

6This is not a typo; Source: Bloomberg, Alphabet Inc 2.25% 2060 as of June 30, 2022

7Source: Bloomberg Barclays US High Yield Corporate Bond Index Yield: trough to peak

8Source: Bloomberg Barclays US Corporate Bond Index Yield: trough to peak

9Source: Bloomberg

10Source: Barclays US Dollar High Yield Corporate Bond Index, Ewing Morris

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Barclays US High Yield Corporate Bond Index Yield and Barclays USCorporate Bond Index Yield as benchmark indices as these are widely known and used benchmark indices for fixedincome markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided forinformation only. Comparisons to benchmarks and indices have limitations. The Fund does not invest in all, ornecessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain,among other things, options, short positions and other securities, concentrated levels of securities and may employleverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund.Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any EwingMorris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meetinvestor suitability and sophistication requirements. While information prepared in this report is believed to beaccurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy norcan it accept responsibility for errors in the report. This report is not intended for public use or distribution. There canbe no guarantee that any projection, forecast or opinion will be realized. All information provided is for informationalpurposes only and should not be construed as personal investment advice. Users of these materials are advised toconduct their own analysis prior to making any investment decision. Source: Capital IQ, Bloomberg and Ewing Morris.As of June 30, 2022.

To the Limited Partners of the Flexible Fixed Income Fund LP,

In the second quarter of 2022, the Flexible Fixed Income Fund returned -8.1%. This compares with our high yield and investment grade corporate bond benchmark returns of -9.4% and -5.1%. Since the Fund’s inception in early 2016, the Fund has delivered a compound annual return of +5.1%.

There’s a simple way to frame what has happened in fixed income markets: by May of this year, the bond market had performed worse than any complete year since 1842. While this period hasn’t (yet) been labeled a “crisis,” we are living through one of the most memorable periods that fixed income investors have seen in a generation. Given this backdrop, it is not a surprise that Fund results on an absolute basis are what should ordinarily be viewed as unacceptable. However, widening the aperture only modestly to an 18-month time period reveals the kind of results our approach can deliver. Over this period, we have preserved capital (Fund down 0.7%), while both of our benchmarks (High Yield Bond Index ETF and Canadian Investment Grade Bond Index ETF) are down 10.5% and 13.1%, respectively1. As the history of the Fund has demonstrated, patches of negative returns tend to be temporary and have been followed by strong subsequent performance. For numerous reasons, we believe we are at the front edge of one of the best times to be a high yield bond investor since the inception of the fund more than six years ago.

What's Happened

Before diving into the current state of the market, we’d like to give you an account of how we’ve managed through this historic time. As we expressed in our Q2 2021 letter, we were preparing for the possibility of inflation pressuring the credit market. We shorted the (record expensive) credit risk of long term corporate bonds on the view that inflation (and its consequent central bank tightening) would ultimately impact stock and credit prices. This hedge was executed on a largely diversified basis and was the greatest contributor to our preservation of capital over the last 18 months.

As we moved through 2022, we have been investing increasingly in Structural Value situations. These are investments where the return of the investment is highly specific to the fine print of a bond’s contract. For much of the last thirty years, yields have been falling and bonds have, for the most part, traded above par. When bonds trade above par, the embedded options (like a change of control put right at a price of 101) have no value. However, over the last nine months, a dramatic increase in interest rates has caused a deep decline in bond prices. With bond prices so discounted, events now present a very valuable source of upside - but only if you’ve found the bond contract with the right fine print. This optionality, coupled with plenty of strategic and private equity ‘dry powder,’ presents an underappreciated opportunity set for bond investors in our view. These types of investments have fared far better than the general market as they tend to be shorter-duration and idiosyncratic in nature. For example, in March we purchased Switch Systems 4.125% Sr. Notes due 2029. Less than four months later2, the high yield market is down 7.5%3, while these bonds have generated a return of +3.8%4 owing to the Structural Value embedded in the bond’s contract in connection with a pending takeover of the company by DigitalBridge Group. We have sharpened our focus on situations with this type of setup and have found many of these investments in convertible bonds of technology companies.

The Tax of Inflation Has Entered the Chat

It took a while to happen, but inflation has finally claimed its most obvious victim: the bond market. Returns have been abysmal and finally reflect to a better degree a fair discount rate that incorporates a higher level of expected inflation. Indeed, this period of reappraisal has been a startling process for government bond investors. Furthermore, this volatility in interest rates has caused an increase in the additional yield investors require to own corporate bonds (also known as the “credit spread”). The result of these two factors (increasing rates and credit spreads) is that corporate bond yields are going up (and prices down) even faster than government bonds of the same maturity.

The combination of increasing government bond yields and increasing credit spreads has had an astonishing impact on long-duration corporate bonds. In the span of half a year, many long-term bonds have fallen by 25-35%. Many would be surprised to know that as of this writing, bonds in Google (a company with $134B in cash and only $28B in debt5) are trading at 66 cents6 on the dollar. What’s more is that we do not even own this bond as we are seeing even better opportunities in the market than this.

Opportunities are Nigh

At this juncture, bonds in just about every facet of the corporate bond market have promise and we will highlight three areas: high yield, investment grade and convertible bonds.

High yield is a good place to illuminate first, with expected yields close to their post-great financial crisis highs. In mid-2021, the high yield market once was at 3.5% in yield. Today it sports a desirable yield that has been closing in on 9%.

We are also frequently finding opportunities in investment grade bonds, where contractual features combined with fundamental changes can produce some surprisingly attractive outcomes, relative to the low credit risk of the investment. A good example of this is shorter-term investment grade bonds. These bonds tend to carry exceptionally low credit risk, yet are priced at large discounts (7-10 points) to par, depending on their coupon. On this theme, we own a modest position in Ryder Systems Inc 1.75% Sr. Notes due 2026. Ryder is a transportation and logistics business that has been subject to an informal offer by a private equity firm, which some might see as having put the company ‘in-play’. If a typical take private transaction were to occur at Ryder, under the rules of the bond contract, the bonds would be worth 101. This would represent an overnight gain of 10 points on an event that would not surprise anyone. In the meantime, we are happy to clip our low-risk 4% yield.

Similar Structural Value opportunities are available, in spades, in the convertible bond market. This is because most of the coupons attached to convertible bonds are less than 1%. Most investors buy convertibles for their equity upside. Since the underlying stocks have gone the opposite way intended(down), convertible bonds are now occupying the bargain bin of the corporate bond market. With no equity option value, their economic characteristics have become more like high yield bonds. But, because their coupons are so low, a bond’s “yield” must be earned over time through price appreciation, ultimately culminating at the maturity of the bond, when a bond receives its par payment. A good example of our Structural Value approach as applied in the convertible space is in Everbridge Inc, a company offering critical event communication and asset monitoring technology. Everbridge’s board has found itself to be in a largely indefensible position against a very strong activist campaign which is pushing for a corporate sale. Our principal position in Everbridge is in its 0.125% Sr. Notes due 12/2024. This is a first-to-mature-bond that is covered by cash sitting on Everbridge’s balance sheet. Given the situation, at an 87-dollar price, this investment has a pleasing 15% upside option to par in the event of a corporate sale. In the case this does not happen, we are harvesting a ~6% yield on a cash-covered bond over a two and a half-year term, largely in the tax-efficient form of capital gains.

Admittedly, with the credit market on its back, one should not hold their breath for a take-private deal. However, this still leaves open the likelihood of strategic transactions producing attractive results in a target company’s bonds. Take Resolute Forest Products for example; this freshly announced deal demonstrates that the option value that exists across the entire bond market is real. At an average price of 85 cents, our portfolio is well-positioned for events like this. In fact, we have already have been monetizing these opportunities to date as we discussed in our Q1 2022 letter to Limited Partners.

The Stock Market’s Boss is the Credit Market

The theory goes that if a company cannot service its interest obligations and repay its debt in full at maturity, it's equity value is worthless. Considering high yield bond yields7 moving from 3.5% to 9% (with the market basically closed today) and investment grade bond yields8 moving from 1.75% to 5%, one might want to check whether the stock market’s expected return has become two to three times more attractive in the last 18 months. We make note of this due to the fact that the S&P 500 is down only 20%year-to-date9. We would also point out that this decline followed a 29% climb in 2021 and an 18% climb in the COVID-riddled year of 2020. Given these facts (and equity’s downward-inflecting earnings outlooks) the prices of stocks appear too high if you are as pessimistic as the corporate bond market.

The Path Forward

While we have a highly uncertain economic (and geopolitical) future, there are scores of solid credit investments on sale today in the market. This, more than anything gives us much optimism as we go forward; and this is not just a feeling. Data show that once the market carries a yield of more than 10%, there is an 88% probability of positive returns, 18 months thereafter10. Those are some great odds.

And we’re not the only ones excited. Famed corporate debt investor, Howard Marks, in a recent interview with the Financial Times said that “today I am starting to behave aggressively.” This stood out to us as Marks is quite a conservative investor. The best example of this conservatism was on display in Marks’s April 6, 2020 memo, where he was quite balanced in his outlook (and even held out his expectation for lower asset prices in April). Marks is certainly not a perma-bull.

There are a lot of scenarios under which higher yielding securities work nicely, particularly relative to the broader stock market. We believe the coming quarter will be host to some of the best entry points yet owing to what will be likely a double-threat of downward inflecting results and a negative reset of corporate outlooks. Despite what could be a tough second quarter earnings season, we keep in mind what Marks said in the same interview which was that “the idea of waiting for the bottom is a terrible idea.” On this basis, we are fully invested in securities that, in our opinion, have lower aggregate risk than the high yield market. This allows us the capacity to become more aggressive if even greater bargains reveal themselves. We look forward to taking advantage of what’s to come on your behalf and we thank you for your continued confidence.

***

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures for more details.

118-Month Cumulative Returns as of June 30, 2022.

23/23/2022-7/13/2022

3iShares US High Yield Bond Index Fund (CAD-Hedged)

4Source: Bloomberg

5Source: Company Financials, Bloomberg

6This is not a typo; Source: Bloomberg, Alphabet Inc 2.25% 2060 as of June 30, 2022

7Source: Bloomberg Barclays US High Yield Corporate Bond Index Yield: trough to peak

8Source: Bloomberg Barclays US Corporate Bond Index Yield: trough to peak

9Source: Bloomberg

10Source: Barclays US Dollar High Yield Corporate Bond Index, Ewing Morris

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Barclays US High Yield Corporate Bond Index Yield and Barclays USCorporate Bond Index Yield as benchmark indices as these are widely known and used benchmark indices for fixedincome markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided forinformation only. Comparisons to benchmarks and indices have limitations. The Fund does not invest in all, ornecessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain,among other things, options, short positions and other securities, concentrated levels of securities and may employleverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund.Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any EwingMorris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meetinvestor suitability and sophistication requirements. While information prepared in this report is believed to beaccurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy norcan it accept responsibility for errors in the report. This report is not intended for public use or distribution. There canbe no guarantee that any projection, forecast or opinion will be realized. All information provided is for informationalpurposes only and should not be construed as personal investment advice. Users of these materials are advised toconduct their own analysis prior to making any investment decision. Source: Capital IQ, Bloomberg and Ewing Morris.As of June 30, 2022.

To the Limited Partners of the Flexible Fixed Income Fund LP,

In the second quarter of 2022, the Flexible Fixed Income Fund returned -8.1%. This compares with our high yield and investment grade corporate bond benchmark returns of -9.4% and -5.1%. Since the Fund’s inception in early 2016, the Fund has delivered a compound annual return of +5.1%.

There’s a simple way to frame what has happened in fixed income markets: by May of this year, the bond market had performed worse than any complete year since 1842. While this period hasn’t (yet) been labeled a “crisis,” we are living through one of the most memorable periods that fixed income investors have seen in a generation. Given this backdrop, it is not a surprise that Fund results on an absolute basis are what should ordinarily be viewed as unacceptable. However, widening the aperture only modestly to an 18-month time period reveals the kind of results our approach can deliver. Over this period, we have preserved capital (Fund down 0.7%), while both of our benchmarks (High Yield Bond Index ETF and Canadian Investment Grade Bond Index ETF) are down 10.5% and 13.1%, respectively1. As the history of the Fund has demonstrated, patches of negative returns tend to be temporary and have been followed by strong subsequent performance. For numerous reasons, we believe we are at the front edge of one of the best times to be a high yield bond investor since the inception of the fund more than six years ago.

What's Happened

Before diving into the current state of the market, we’d like to give you an account of how we’ve managed through this historic time. As we expressed in our Q2 2021 letter, we were preparing for the possibility of inflation pressuring the credit market. We shorted the (record expensive) credit risk of long term corporate bonds on the view that inflation (and its consequent central bank tightening) would ultimately impact stock and credit prices. This hedge was executed on a largely diversified basis and was the greatest contributor to our preservation of capital over the last 18 months.

As we moved through 2022, we have been investing increasingly in Structural Value situations. These are investments where the return of the investment is highly specific to the fine print of a bond’s contract. For much of the last thirty years, yields have been falling and bonds have, for the most part, traded above par. When bonds trade above par, the embedded options (like a change of control put right at a price of 101) have no value. However, over the last nine months, a dramatic increase in interest rates has caused a deep decline in bond prices. With bond prices so discounted, events now present a very valuable source of upside - but only if you’ve found the bond contract with the right fine print. This optionality, coupled with plenty of strategic and private equity ‘dry powder,’ presents an underappreciated opportunity set for bond investors in our view. These types of investments have fared far better than the general market as they tend to be shorter-duration and idiosyncratic in nature. For example, in March we purchased Switch Systems 4.125% Sr. Notes due 2029. Less than four months later2, the high yield market is down 7.5%3, while these bonds have generated a return of +3.8%4 owing to the Structural Value embedded in the bond’s contract in connection with a pending takeover of the company by DigitalBridge Group. We have sharpened our focus on situations with this type of setup and have found many of these investments in convertible bonds of technology companies.

The Tax of Inflation Has Entered the Chat

It took a while to happen, but inflation has finally claimed its most obvious victim: the bond market. Returns have been abysmal and finally reflect to a better degree a fair discount rate that incorporates a higher level of expected inflation. Indeed, this period of reappraisal has been a startling process for government bond investors. Furthermore, this volatility in interest rates has caused an increase in the additional yield investors require to own corporate bonds (also known as the “credit spread”). The result of these two factors (increasing rates and credit spreads) is that corporate bond yields are going up (and prices down) even faster than government bonds of the same maturity.

The combination of increasing government bond yields and increasing credit spreads has had an astonishing impact on long-duration corporate bonds. In the span of half a year, many long-term bonds have fallen by 25-35%. Many would be surprised to know that as of this writing, bonds in Google (a company with $134B in cash and only $28B in debt5) are trading at 66 cents6 on the dollar. What’s more is that we do not even own this bond as we are seeing even better opportunities in the market than this.

Opportunities are Nigh

At this juncture, bonds in just about every facet of the corporate bond market have promise and we will highlight three areas: high yield, investment grade and convertible bonds.

High yield is a good place to illuminate first, with expected yields close to their post-great financial crisis highs. In mid-2021, the high yield market once was at 3.5% in yield. Today it sports a desirable yield that has been closing in on 9%.

We are also frequently finding opportunities in investment grade bonds, where contractual features combined with fundamental changes can produce some surprisingly attractive outcomes, relative to the low credit risk of the investment. A good example of this is shorter-term investment grade bonds. These bonds tend to carry exceptionally low credit risk, yet are priced at large discounts (7-10 points) to par, depending on their coupon. On this theme, we own a modest position in Ryder Systems Inc 1.75% Sr. Notes due 2026. Ryder is a transportation and logistics business that has been subject to an informal offer by a private equity firm, which some might see as having put the company ‘in-play’. If a typical take private transaction were to occur at Ryder, under the rules of the bond contract, the bonds would be worth 101. This would represent an overnight gain of 10 points on an event that would not surprise anyone. In the meantime, we are happy to clip our low-risk 4% yield.

Similar Structural Value opportunities are available, in spades, in the convertible bond market. This is because most of the coupons attached to convertible bonds are less than 1%. Most investors buy convertibles for their equity upside. Since the underlying stocks have gone the opposite way intended(down), convertible bonds are now occupying the bargain bin of the corporate bond market. With no equity option value, their economic characteristics have become more like high yield bonds. But, because their coupons are so low, a bond’s “yield” must be earned over time through price appreciation, ultimately culminating at the maturity of the bond, when a bond receives its par payment. A good example of our Structural Value approach as applied in the convertible space is in Everbridge Inc, a company offering critical event communication and asset monitoring technology. Everbridge’s board has found itself to be in a largely indefensible position against a very strong activist campaign which is pushing for a corporate sale. Our principal position in Everbridge is in its 0.125% Sr. Notes due 12/2024. This is a first-to-mature-bond that is covered by cash sitting on Everbridge’s balance sheet. Given the situation, at an 87-dollar price, this investment has a pleasing 15% upside option to par in the event of a corporate sale. In the case this does not happen, we are harvesting a ~6% yield on a cash-covered bond over a two and a half-year term, largely in the tax-efficient form of capital gains.

Admittedly, with the credit market on its back, one should not hold their breath for a take-private deal. However, this still leaves open the likelihood of strategic transactions producing attractive results in a target company’s bonds. Take Resolute Forest Products for example; this freshly announced deal demonstrates that the option value that exists across the entire bond market is real. At an average price of 85 cents, our portfolio is well-positioned for events like this. In fact, we have already have been monetizing these opportunities to date as we discussed in our Q1 2022 letter to Limited Partners.

The Stock Market’s Boss is the Credit Market

The theory goes that if a company cannot service its interest obligations and repay its debt in full at maturity, it's equity value is worthless. Considering high yield bond yields7 moving from 3.5% to 9% (with the market basically closed today) and investment grade bond yields8 moving from 1.75% to 5%, one might want to check whether the stock market’s expected return has become two to three times more attractive in the last 18 months. We make note of this due to the fact that the S&P 500 is down only 20%year-to-date9. We would also point out that this decline followed a 29% climb in 2021 and an 18% climb in the COVID-riddled year of 2020. Given these facts (and equity’s downward-inflecting earnings outlooks) the prices of stocks appear too high if you are as pessimistic as the corporate bond market.

The Path Forward

While we have a highly uncertain economic (and geopolitical) future, there are scores of solid credit investments on sale today in the market. This, more than anything gives us much optimism as we go forward; and this is not just a feeling. Data show that once the market carries a yield of more than 10%, there is an 88% probability of positive returns, 18 months thereafter10. Those are some great odds.

And we’re not the only ones excited. Famed corporate debt investor, Howard Marks, in a recent interview with the Financial Times said that “today I am starting to behave aggressively.” This stood out to us as Marks is quite a conservative investor. The best example of this conservatism was on display in Marks’s April 6, 2020 memo, where he was quite balanced in his outlook (and even held out his expectation for lower asset prices in April). Marks is certainly not a perma-bull.

There are a lot of scenarios under which higher yielding securities work nicely, particularly relative to the broader stock market. We believe the coming quarter will be host to some of the best entry points yet owing to what will be likely a double-threat of downward inflecting results and a negative reset of corporate outlooks. Despite what could be a tough second quarter earnings season, we keep in mind what Marks said in the same interview which was that “the idea of waiting for the bottom is a terrible idea.” On this basis, we are fully invested in securities that, in our opinion, have lower aggregate risk than the high yield market. This allows us the capacity to become more aggressive if even greater bargains reveal themselves. We look forward to taking advantage of what’s to come on your behalf and we thank you for your continued confidence.

***

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures for more details.

118-Month Cumulative Returns as of June 30, 2022.

23/23/2022-7/13/2022

3iShares US High Yield Bond Index Fund (CAD-Hedged)

4Source: Bloomberg

5Source: Company Financials, Bloomberg

6This is not a typo; Source: Bloomberg, Alphabet Inc 2.25% 2060 as of June 30, 2022

7Source: Bloomberg Barclays US High Yield Corporate Bond Index Yield: trough to peak

8Source: Bloomberg Barclays US Corporate Bond Index Yield: trough to peak

9Source: Bloomberg

10Source: Barclays US Dollar High Yield Corporate Bond Index, Ewing Morris

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Barclays US High Yield Corporate Bond Index Yield and Barclays USCorporate Bond Index Yield as benchmark indices as these are widely known and used benchmark indices for fixedincome markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided forinformation only. Comparisons to benchmarks and indices have limitations. The Fund does not invest in all, ornecessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain,among other things, options, short positions and other securities, concentrated levels of securities and may employleverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund.Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any EwingMorris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meetinvestor suitability and sophistication requirements. While information prepared in this report is believed to beaccurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy norcan it accept responsibility for errors in the report. This report is not intended for public use or distribution. There canbe no guarantee that any projection, forecast or opinion will be realized. All information provided is for informationalpurposes only and should not be construed as personal investment advice. Users of these materials are advised toconduct their own analysis prior to making any investment decision. Source: Capital IQ, Bloomberg and Ewing Morris.As of June 30, 2022.

To the Limited Partners of the Flexible Fixed Income Fund LP,

In the second quarter of 2022, the Flexible Fixed Income Fund returned -8.1%. This compares with our high yield and investment grade corporate bond benchmark returns of -9.4% and -5.1%. Since the Fund’s inception in early 2016, the Fund has delivered a compound annual return of +5.1%.

There’s a simple way to frame what has happened in fixed income markets: by May of this year, the bond market had performed worse than any complete year since 1842. While this period hasn’t (yet) been labeled a “crisis,” we are living through one of the most memorable periods that fixed income investors have seen in a generation. Given this backdrop, it is not a surprise that Fund results on an absolute basis are what should ordinarily be viewed as unacceptable. However, widening the aperture only modestly to an 18-month time period reveals the kind of results our approach can deliver. Over this period, we have preserved capital (Fund down 0.7%), while both of our benchmarks (High Yield Bond Index ETF and Canadian Investment Grade Bond Index ETF) are down 10.5% and 13.1%, respectively1. As the history of the Fund has demonstrated, patches of negative returns tend to be temporary and have been followed by strong subsequent performance. For numerous reasons, we believe we are at the front edge of one of the best times to be a high yield bond investor since the inception of the fund more than six years ago.

What's Happened

Before diving into the current state of the market, we’d like to give you an account of how we’ve managed through this historic time. As we expressed in our Q2 2021 letter, we were preparing for the possibility of inflation pressuring the credit market. We shorted the (record expensive) credit risk of long term corporate bonds on the view that inflation (and its consequent central bank tightening) would ultimately impact stock and credit prices. This hedge was executed on a largely diversified basis and was the greatest contributor to our preservation of capital over the last 18 months.

As we moved through 2022, we have been investing increasingly in Structural Value situations. These are investments where the return of the investment is highly specific to the fine print of a bond’s contract. For much of the last thirty years, yields have been falling and bonds have, for the most part, traded above par. When bonds trade above par, the embedded options (like a change of control put right at a price of 101) have no value. However, over the last nine months, a dramatic increase in interest rates has caused a deep decline in bond prices. With bond prices so discounted, events now present a very valuable source of upside - but only if you’ve found the bond contract with the right fine print. This optionality, coupled with plenty of strategic and private equity ‘dry powder,’ presents an underappreciated opportunity set for bond investors in our view. These types of investments have fared far better than the general market as they tend to be shorter-duration and idiosyncratic in nature. For example, in March we purchased Switch Systems 4.125% Sr. Notes due 2029. Less than four months later2, the high yield market is down 7.5%3, while these bonds have generated a return of +3.8%4 owing to the Structural Value embedded in the bond’s contract in connection with a pending takeover of the company by DigitalBridge Group. We have sharpened our focus on situations with this type of setup and have found many of these investments in convertible bonds of technology companies.

The Tax of Inflation Has Entered the Chat

It took a while to happen, but inflation has finally claimed its most obvious victim: the bond market. Returns have been abysmal and finally reflect to a better degree a fair discount rate that incorporates a higher level of expected inflation. Indeed, this period of reappraisal has been a startling process for government bond investors. Furthermore, this volatility in interest rates has caused an increase in the additional yield investors require to own corporate bonds (also known as the “credit spread”). The result of these two factors (increasing rates and credit spreads) is that corporate bond yields are going up (and prices down) even faster than government bonds of the same maturity.

The combination of increasing government bond yields and increasing credit spreads has had an astonishing impact on long-duration corporate bonds. In the span of half a year, many long-term bonds have fallen by 25-35%. Many would be surprised to know that as of this writing, bonds in Google (a company with $134B in cash and only $28B in debt5) are trading at 66 cents6 on the dollar. What’s more is that we do not even own this bond as we are seeing even better opportunities in the market than this.

Opportunities are Nigh

At this juncture, bonds in just about every facet of the corporate bond market have promise and we will highlight three areas: high yield, investment grade and convertible bonds.

High yield is a good place to illuminate first, with expected yields close to their post-great financial crisis highs. In mid-2021, the high yield market once was at 3.5% in yield. Today it sports a desirable yield that has been closing in on 9%.

We are also frequently finding opportunities in investment grade bonds, where contractual features combined with fundamental changes can produce some surprisingly attractive outcomes, relative to the low credit risk of the investment. A good example of this is shorter-term investment grade bonds. These bonds tend to carry exceptionally low credit risk, yet are priced at large discounts (7-10 points) to par, depending on their coupon. On this theme, we own a modest position in Ryder Systems Inc 1.75% Sr. Notes due 2026. Ryder is a transportation and logistics business that has been subject to an informal offer by a private equity firm, which some might see as having put the company ‘in-play’. If a typical take private transaction were to occur at Ryder, under the rules of the bond contract, the bonds would be worth 101. This would represent an overnight gain of 10 points on an event that would not surprise anyone. In the meantime, we are happy to clip our low-risk 4% yield.

Similar Structural Value opportunities are available, in spades, in the convertible bond market. This is because most of the coupons attached to convertible bonds are less than 1%. Most investors buy convertibles for their equity upside. Since the underlying stocks have gone the opposite way intended(down), convertible bonds are now occupying the bargain bin of the corporate bond market. With no equity option value, their economic characteristics have become more like high yield bonds. But, because their coupons are so low, a bond’s “yield” must be earned over time through price appreciation, ultimately culminating at the maturity of the bond, when a bond receives its par payment. A good example of our Structural Value approach as applied in the convertible space is in Everbridge Inc, a company offering critical event communication and asset monitoring technology. Everbridge’s board has found itself to be in a largely indefensible position against a very strong activist campaign which is pushing for a corporate sale. Our principal position in Everbridge is in its 0.125% Sr. Notes due 12/2024. This is a first-to-mature-bond that is covered by cash sitting on Everbridge’s balance sheet. Given the situation, at an 87-dollar price, this investment has a pleasing 15% upside option to par in the event of a corporate sale. In the case this does not happen, we are harvesting a ~6% yield on a cash-covered bond over a two and a half-year term, largely in the tax-efficient form of capital gains.

Admittedly, with the credit market on its back, one should not hold their breath for a take-private deal. However, this still leaves open the likelihood of strategic transactions producing attractive results in a target company’s bonds. Take Resolute Forest Products for example; this freshly announced deal demonstrates that the option value that exists across the entire bond market is real. At an average price of 85 cents, our portfolio is well-positioned for events like this. In fact, we have already have been monetizing these opportunities to date as we discussed in our Q1 2022 letter to Limited Partners.

The Stock Market’s Boss is the Credit Market

The theory goes that if a company cannot service its interest obligations and repay its debt in full at maturity, it's equity value is worthless. Considering high yield bond yields7 moving from 3.5% to 9% (with the market basically closed today) and investment grade bond yields8 moving from 1.75% to 5%, one might want to check whether the stock market’s expected return has become two to three times more attractive in the last 18 months. We make note of this due to the fact that the S&P 500 is down only 20%year-to-date9. We would also point out that this decline followed a 29% climb in 2021 and an 18% climb in the COVID-riddled year of 2020. Given these facts (and equity’s downward-inflecting earnings outlooks) the prices of stocks appear too high if you are as pessimistic as the corporate bond market.

The Path Forward

While we have a highly uncertain economic (and geopolitical) future, there are scores of solid credit investments on sale today in the market. This, more than anything gives us much optimism as we go forward; and this is not just a feeling. Data show that once the market carries a yield of more than 10%, there is an 88% probability of positive returns, 18 months thereafter10. Those are some great odds.

And we’re not the only ones excited. Famed corporate debt investor, Howard Marks, in a recent interview with the Financial Times said that “today I am starting to behave aggressively.” This stood out to us as Marks is quite a conservative investor. The best example of this conservatism was on display in Marks’s April 6, 2020 memo, where he was quite balanced in his outlook (and even held out his expectation for lower asset prices in April). Marks is certainly not a perma-bull.

There are a lot of scenarios under which higher yielding securities work nicely, particularly relative to the broader stock market. We believe the coming quarter will be host to some of the best entry points yet owing to what will be likely a double-threat of downward inflecting results and a negative reset of corporate outlooks. Despite what could be a tough second quarter earnings season, we keep in mind what Marks said in the same interview which was that “the idea of waiting for the bottom is a terrible idea.” On this basis, we are fully invested in securities that, in our opinion, have lower aggregate risk than the high yield market. This allows us the capacity to become more aggressive if even greater bargains reveal themselves. We look forward to taking advantage of what’s to come on your behalf and we thank you for your continued confidence.

***

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures for more details.

118-Month Cumulative Returns as of June 30, 2022.

23/23/2022-7/13/2022

3iShares US High Yield Bond Index Fund (CAD-Hedged)

4Source: Bloomberg

5Source: Company Financials, Bloomberg

6This is not a typo; Source: Bloomberg, Alphabet Inc 2.25% 2060 as of June 30, 2022

7Source: Bloomberg Barclays US High Yield Corporate Bond Index Yield: trough to peak

8Source: Bloomberg Barclays US Corporate Bond Index Yield: trough to peak

9Source: Bloomberg

10Source: Barclays US Dollar High Yield Corporate Bond Index, Ewing Morris

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Barclays US High Yield Corporate Bond Index Yield and Barclays USCorporate Bond Index Yield as benchmark indices as these are widely known and used benchmark indices for fixedincome markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided forinformation only. Comparisons to benchmarks and indices have limitations. The Fund does not invest in all, ornecessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain,among other things, options, short positions and other securities, concentrated levels of securities and may employleverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund.Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any EwingMorris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meetinvestor suitability and sophistication requirements. While information prepared in this report is believed to beaccurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy norcan it accept responsibility for errors in the report. This report is not intended for public use or distribution. There canbe no guarantee that any projection, forecast or opinion will be realized. All information provided is for informationalpurposes only and should not be construed as personal investment advice. Users of these materials are advised toconduct their own analysis prior to making any investment decision. Source: Capital IQ, Bloomberg and Ewing Morris.As of June 30, 2022.

2022 Annual Letter

To the Limited Partners of the Ewing Morris Flexible Fixed Income Fund:

Our Performance in 2022

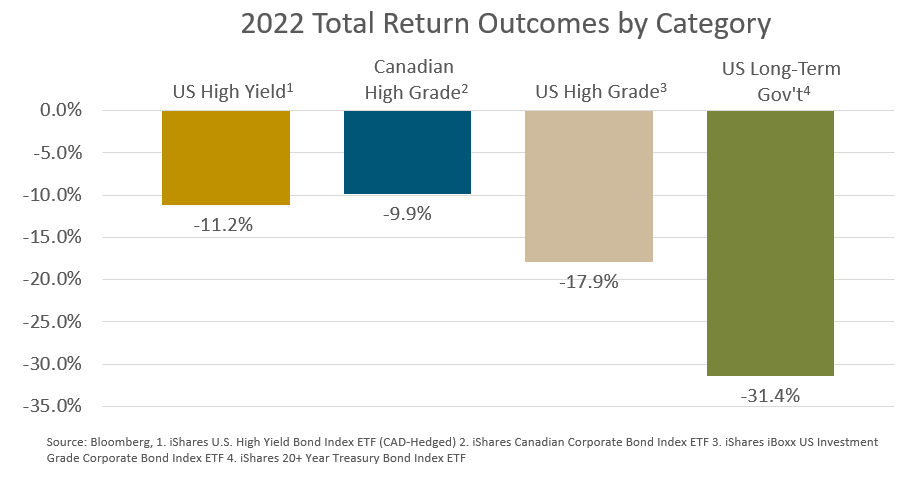

In 2022, the Flexible Fixed Income Fund Returned -4.7%. This return compares to our publicly traded high yield and investment grade benchmarks, which in 2022 returned -11.2% and -9.9% respectively.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of December 31, 2022. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF(CAD-Hedged). Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF.

Everyone knows what happened in2022. Interest rates soared and many argue that we have crossed the Rubicon into a new geopolitical, economic and monetary regime. It was the worst year for bonds in a generation.

Having lost money in 2022, we cannot help but to be disappointed with the outcome in absolute terms. The counterbalance to this is the Fund outperformed its benchmark by 6.5 percentage points – the largest gap in the history of the fund. We can also put this relative performance in an absolute return context - since the inception of the high yield market index, 36 years ago, a 6.5 percentage point value-add would have been sufficient to produce a positive absolute return in any calendar year other than 2008. In a phrase, the year was “passable but insufficient.”

Performance: Puts and Takes

Performance detractors were, unsurprisingly, broad-based as even short-term risk-free bonds suffered in price1. However, the convertible bond sector is where the fund saw its largest individual losses. As we have found great promise in the convertible bond market in 2022, about 40% of fund capital is invested in this space. With a number of investments in this space, there were negative contributors. In one case, we misjudged management’s orientation toward creditors (Dye & Durham, which cost the fund 1.0%). In another case, we bought what we believe is an eventual par outcome at a purchase price in the low 70’s, only to see the convertible sink into the mid 50’s on tightness in funding markets and consumer concerns (Affirm, which cost the fund 1.2%). And, in another case the decline of a convertible bond that has immense long-term equity optionality to levels we believe are exceptionally cheap (Ziff Davis, which cost the fund 1.2%). In sum, positions in these three companies detracted 3.5 percentage points of return. And, when including Coinbase (which still sports zero net debt and bonds in the 50’s), the rake-stepping tally rises into the 5% range. Your Portfolio Manager will not offer any excuses for these negative outcomes.

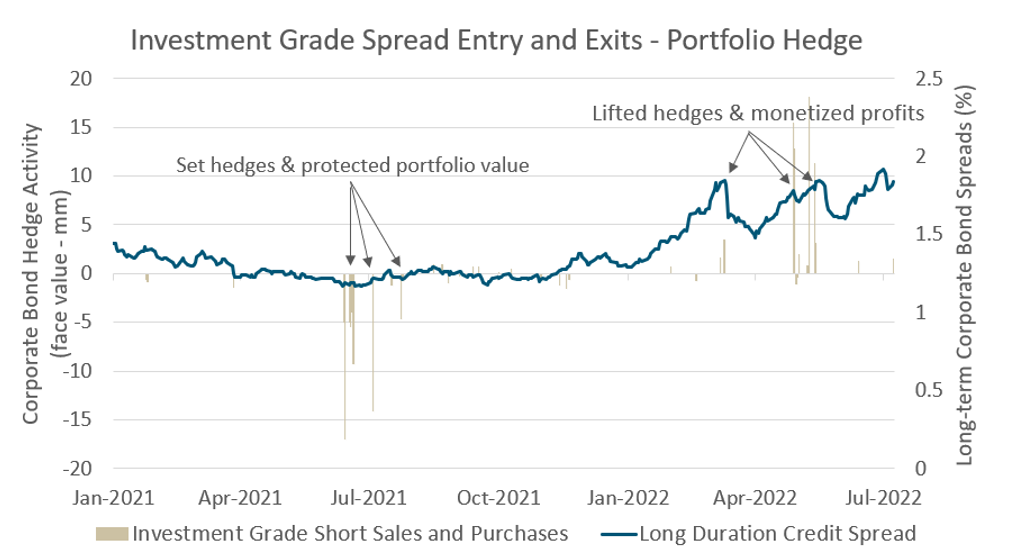

The greatest positive single contributor to results in 2022 was a broad credit hedge we put in place in Q3 of 2021, which paid off in the first half of the year as rates shot up and high-grade credit markets weakened. In 2021, we identified the possibility that inflation may end up pressuring the credit market, which at the time carried prices that implied very little expectation of future inflation (or even economic weakness). Seeing this setup as a near “free” option to insulate the portfolio from stormy financial conditions, we shorted the (record expensive) credit risk of long-term corporate bonds on the view that inflation (and its consequent central bank tightening) would ultimately impact stock and credit prices. This hedge was executed on a diversified basis (largely through electronic ‘portfolio trades’) and was the greatest contributor to our preservation of capital from 2021 to mid 2022. In 2022, this position added 5.2 percentage points of return to the fund.

We also saw success in 2022 in our Structural Value investments. These are investments where the investment outcome is driven by features of the bond contract rather than by business performance or its management team’s credit stewardship.

Profitable investing requires asymmetry. Asymmetry in information and asymmetry in insight are conditions for potential asymmetry in investment outcome. We are seeing Structural Value positions tied to corporate events as an investment category that is among the most asymmetry-rich spaces that we can find in the market. For a variety of circumstances, companies from time-to-time consider corporate events such as reorganizations, mergers or sales, which can have profound implications on their bonds. The economic consequences to the bonds are driven by what’s contained in each bond contract. Recognizing and monetizing this type of opportunity requires integrating governance-based pattern recognition, real-world industrial logic and debt contract analysis. Without this analytical combination, a bond may appear like any other when - in substance - it is not.

Although the total profit pool of this investment category is substantial, the problem is that it requires decision makers to personally have (or have immediately available to them) this disparate combination of skillsets. Because of this challenge, this event-driven profit pool is not a focal point for large fixed income managers. The interesting question is “Why”? As a practical matter in a race to the bottom on fees, the average capital deployed per investment professional has ballooned over time, forcing fixed income asset manager research departments to focus only on the most readily accessible profit pools, being credit quality, duration and sector. Compounding this theme, large asset managers are increasingly managing their portfolios through electronic venues and more commonly using “portfolio trades”, targeting baskets of a specified credit quality, duration and sector. Under this approach, special situations in any specific bond in the basket does not matter as much to a decision maker as the characteristic and pricing of the basket that is being traded.

This dynamic opens the opportunity for asymmetric engagement in markets of corporate debt securities. This became strikingly apparent to us in certain situations we monetized in 2021, the Shaw Communication Preferred Shares2 being the standout example of this. We dedicated significant resources to this area in 2022 due to its profitability and continued promise in a fixed income landscape that is becoming more quantitatively driven.

Bond trading has clearly turned more electronic (as opposed to in Bloomberg chat or over the phone). We have noticed a marked increase in the prevalence of automated pricing and algorithm-driven counterparties on electronic trading venues. These players often trade based on descriptive statistics and relative value of a bond. If this is the case, this trend may actually deepen this event-driven profit pool in the future. We look forward to finding out.

The Current Situation

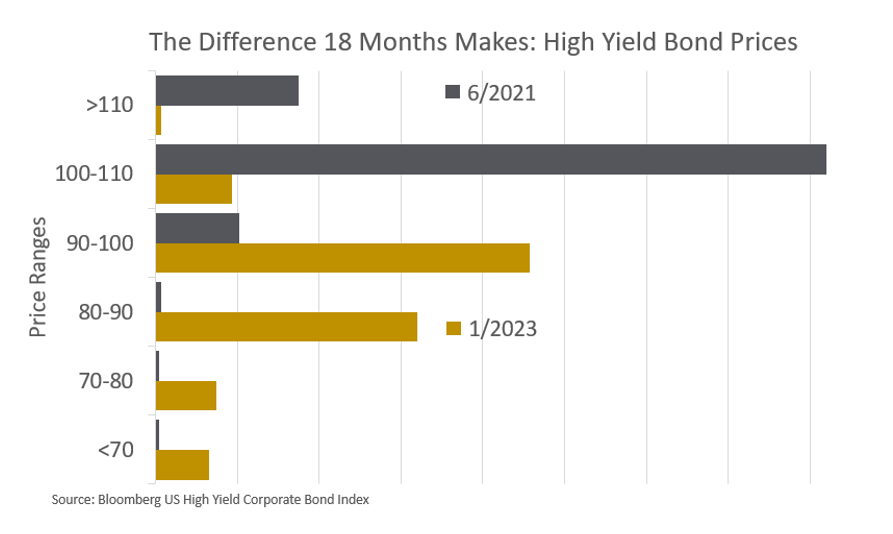

For the first time in more than a decade, we are seeing a sustained and strikingly wide range in pricing in the bond market. One needs to look no further than some bonds of Google, which trade at 60 cents on the dollar to find proof of this3. It’s not lost upon us that swathes of high yield and high-grade bonds are now trading at “recovery value” prices, despite good credit quality. Due to the swift move higher in yields, the current situation is one that we have scarcely seen in the history of corporate bond markets. As the below figure shows, the overwhelming majority of bonds in 2021 were found in the 100-110 price range. Today the most common bond prices start with an ‘8’ or a ‘9’. There are also more bonds priced below 80 than there are bonds priced above par (100). Up until 2022, the bond market was a fairly simple offering - chocolate or vanilla. Today, the market is a veritable Baskin Robbins and we are active, scoop and waffle cones in hand.

A Note on Our Fixed Income Investment Operation

In a year like 2022, it is easy to become captive to market moves and macro narratives, which threaten to distract us from keeping the main thing the main thing. To guard against getting carried away by these dynamics, we remind ourselves of the essence of our task at hand. This reminder may be also helpful to you. In its most simple form, our operation buys claims on North American business. We exchange capital today for well-defined promises of the repayment of more capital tomorrow. These promises are debt contracts backed by North American business. Importantly, the promises that we buy do not require the financial success of a business. These promises simply require a lack of failure. The debt contracts of these businesses trade in the market at prices that the market sets on any given day. Importantly, prices for individual debt contracts occasionally become divorced from their true value. This “dislocation” tends to be driven by inaccurate assessments of the business’ resilience, people running or governing the business or the contractual features of the debt itself. Sometimes dislocations are even more simple, when the owners of the debt contracts see what everyone else sees, but nonetheless have to sell the debt anyway. Regardless of circumstance, it is our job to accurately identify truly dislocated situations and make informed purchases and sales based on our investment insight. Your financial success with us will be defined by the accuracy of our decisions. If the cumulative accuracy of our decisions is superior, results will exceed our fixed income benchmarks over the long-term. It should be noted that it is possible for performance track records to deviate from underlying skill. However, as time passes, Bill Parcells’s4 message on track record becomes indisputable: “You are what your record says you are.”

Outlook

As of this writing, the high yield default cycle has yet to truly arrive. Many observers are calling for rough performance in the asset class on account of their view that the additional yield high yield bonds offer over risk free government bonds (known as the credit spread) is insufficient. We very much appreciate this perspective and even after the strong start to the year (+3.4%)5 we wouldn’t be surprised to see the asset class down in moments in 2023, perhaps materially. However, in a circumstance such as this where high yield finds itself back near or into double digit yield territory (from it’s current 8% level), we would likely view this as an opportunity of a cycle. However, expecting or betting on that to happen is to discount the history of high yield performance. It is striking to note that high yield bonds have never seen consecutive down (calendar) years in its recorded history. As the opportunity set is strong and it is impossible to predict the zig-zags of the market, we remain fully invested and are ready to deploy capital with agility when situations and market circumstances justify.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

1 Source: Bloomberg - sample short-term US Treasury Note (ie: T 1.5% due 11/2024) returned negative 5.5% in 2022.

2Average purchase price of $19.71 (post-announcement) versus redemption price of $25.00

3Source: Bloomberg - GOOGL 2.25% due 2060. These notes traded as low as 52 cents in 2022.

4Bill Parcells: the only NFL coach to lead four different franchises to the playoffs and three to a conference championship game. In four years, he lead the New York Giants - a team that when he joined had only one year with a winning record in their last ten - to win a Super Bowl championship.

5As of January 17, 2023

Schedule a

Conversation

Connect with Peers

Explore Our Full Library

Library

Minimizing Tax Drag (Part 2)