Fellow Limited Partners,

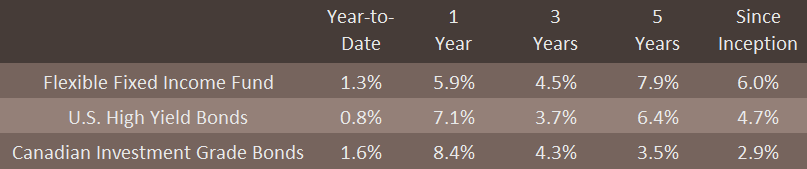

In the first quarter of 2025, the Flexible Fixed Income Fund returned +1.3%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and +1.6%,respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.0%, meeting our long-term net return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

While it is easy to expect the world and markets to unfold in a straightforward progression, on occasion, reality brings something different. This year certainly has - from non-linear policy changes to non-linear market reactions.

The Yield is High Again

A defenestration of long-held economic and state doctrine by current US leadership has marked the beginning of something valuable: higher yields. 2025 (and 2026 for that matter) may turn out to be one of the most opportunity-rich years we have seen in a long time. Of course, we do not know for certain if these years will be high returning, but what we do know is that when uncertainty reigns, returns tend to follow, especially in high yield bonds.

In the corporate bond market, two important things have happened. First, in the United States, interest rates for US Treasury bonds have risen substantially on questions regarding the safe-haven status of US assets. This is not a welcome development for US policymakers and might be a step-change that produces a long-term tailwind for fixed income returns. Second, there has been a spike in credit spreads in anticipation of a more difficult economic environment ahead. These two factors have combined to push high yield bond yields back to levels that reflect emerging concerns of recession. This makes the opportunity set more interesting, not less. We are looking forward to the year ahead.

Timely Tax Takeaways

As tax season is upon us, you might welcome something positive on this topic. As the substantial majority of our investors are tax-paying individuals and families, we believe it is our duty to incorporate an after-tax mindset in our bond investment activity. To our delight, we have observed that the market largely does not differentiate between bonds based on their tax characteristics. Naturally, we have been capitalizing on this dynamic for you since the Fund’s inception, more than nine years ago.

The essence of this tax-aware mindset is to favor bonds issued with low interest rates (a low “coupon”). Since market yields change, bond prices also change to reflect a new fair rate of return. This means bonds with very low, below-market coupons tend to be priced at attractive discounts to par. The lower a bond’s coupon, the higher the price discount. Through this price discount, a bond’s return becomes more valuable. A bond priced at a discount earns its return not only through its coupon, but (importantly) through the gradual appreciation of its price to par maturity. And the greater the price discount, the greater proportion of the bond’s total return will be generated from the bond’s price appreciation. This price appreciation is counted as a capital gain, which bears substantially more favorable tax treatment than ordinary interest income. In an asset class that sweats over basis points (one-hundredths of a percent), this is a highly valuable nuance for taxable clients. And while this approach produces no difference to the pre-tax results you see on the facing page of this letter, it certainly makes a difference to your bank account and in a few other ways which we will share.

Tax Deferral: Taxes on interest income are paid annually as the income is received, so a traditional, high-coupon bond results in a higher tax bill every year. By contrast, a low-coupon, discounted bond gradually moving to par incurs little tax until the year of its sale (or its maturity), effectively postponing much of the tax impact, better compounding an investment’s value.

Success-Based Taxes: Taxes on capital gains are owed only if the bond is sold at a profit. When the bulk of an investment’s expected return comes from price appreciation, this is advantageous. Capital gains tax is, by definition, contingent on the success of the investment. On the other hand, high-coupon bonds generate taxable interest every year, even if the bond later loses value or – even worse – the company goes bankrupt.

Safer Return Generation: Since higher yields typically mean higher credit risk, we are always seeking more conservative ways to achieve safer after-tax returns. By taking advantage of the tax benefits of discounted, low-coupon bonds, we can often match the after-tax return of a higher-yield, higher-risk bond, through a substantially lower-risk company.

Pleasant Surprises: Another benefit comes from company takeovers. Each year, it’s not unusual for four to five percent of public companies to be delisted due to mergers or acquisitions. When this happens, their bonds are very often paid off at par or better. Discounted bonds, in these cases, contain a “hidden bonus” - the chance for an immediate and positive jump in value if such an event occurs. We should add that this value is not theoretical – we experienced two of these events in the portfolio just last year.

Where Flexibility Counts

While this concept is simple, we have taken it very seriously. We have applied this lens as we’ve scoured the market for opportunities. Fortunately, we found an excellent base for tax-advantaged idea generation: the US convertible bond market. These bonds (which must be paid in cash at their maturity unlike their Canadian counterparts) typically bear coupons between zero and two percent and have five-year terms. This US$300 billion-dollar market trades primarily over equity or equity derivative desks, putting it outside the scope of convenience for traditional fixed income investors. We also like that, given the number of issuers (~500), at any given time there are convertible bond issuers that are amid some adversity or mispricing. We have shared convertible bond case studies to highlight this attractive space in prior communications. In sum, our activity in this fixed income market niche is an excellent example of how we use our flexible mandate to generate quality risk-adjusted returns.

So why doesn’t everyone else focus on low coupon bonds? The reasons are many.

Clients: The investment management industry – fixed income in particular - has very substantial customers in pensions, endowments and foundations. These entities are the often the largest and most popular organizations to service. These entities are tax-exempt, so they do not care about the sources of return. Investment managers who count these entities as large clients (almost any manager of scale) may naturally jettison tax considerations as well.

Marketing: Because of the multi-faceted nature of taxes and varying individual tax rates, it is not particularly easy to communicate results with respect to tax. In addition, since pre-tax returns are the industry standard basis of competition, it should not be a surprise that many managers simply optimize for ‘headline’ (pre-tax) fund returns.

Size: For large asset managers (which most fixed income managers are), capital is always required to be put to work. This often presents a problem, where a manager is very much constrained by what’s available in the market. What is available isn’t always economically convenient. Indeed, there are numerous examples of highly liquid bonds in the market having average (or worse) tax characteristics.

Fortunately, we are largely free (or unbothered by) these constraints and have taken full advantage of this for you. If you are interested in your individual mix of taxable gains, we would be delighted to connect on this.

Outlook

It has taken a wholesale change in fiscal, foreign and trade policies, but fixed income is once again pricing in a good portion of the uncertainty many feel about the future. As of this writing, while not at extreme levels, the market has moved to the pessimistic side of the sentiment ledger. This should be welcomed; the more pessimism that is reflected in a bond’s price, the safer an investment it tends to become.

With this recent change in overall attractiveness of the bond market, we have been active in taking advantage of better expected returns in the market, boosting the portfolio’s overall yield through the reduction of hedges and the addition of new credits in the fund. Despite this activity, our positioning remains ‘below market’ in terms of credit risk. Plenty of sand, wrenches and all-caps tweets have been thrown into the gears of the world economy. Perhaps we have already seen “peak uncertainty”, but it also remains to be seen whether we are past “peak pain”. It is impossible to know. This is why we regularly remind ourselves that the only job of economic or market forecasting is to make astrology look respectable. In contrast, our job is simple: find great opportunities come rain or shine, one investment at a time.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg USCorporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these arewidely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investmentmandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks andindices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Funddoes not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and theFund portfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source for datareferenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2025.

Fellow Limited Partners,

In the first quarter of 2025, the Flexible Fixed Income Fund returned +1.3%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and +1.6%,respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.0%, meeting our long-term net return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

While it is easy to expect the world and markets to unfold in a straightforward progression, on occasion, reality brings something different. This year certainly has - from non-linear policy changes to non-linear market reactions.

The Yield is High Again

A defenestration of long-held economic and state doctrine by current US leadership has marked the beginning of something valuable: higher yields. 2025 (and 2026 for that matter) may turn out to be one of the most opportunity-rich years we have seen in a long time. Of course, we do not know for certain if these years will be high returning, but what we do know is that when uncertainty reigns, returns tend to follow, especially in high yield bonds.

In the corporate bond market, two important things have happened. First, in the United States, interest rates for US Treasury bonds have risen substantially on questions regarding the safe-haven status of US assets. This is not a welcome development for US policymakers and might be a step-change that produces a long-term tailwind for fixed income returns. Second, there has been a spike in credit spreads in anticipation of a more difficult economic environment ahead. These two factors have combined to push high yield bond yields back to levels that reflect emerging concerns of recession. This makes the opportunity set more interesting, not less. We are looking forward to the year ahead.

Timely Tax Takeaways

As tax season is upon us, you might welcome something positive on this topic. As the substantial majority of our investors are tax-paying individuals and families, we believe it is our duty to incorporate an after-tax mindset in our bond investment activity. To our delight, we have observed that the market largely does not differentiate between bonds based on their tax characteristics. Naturally, we have been capitalizing on this dynamic for you since the Fund’s inception, more than nine years ago.

The essence of this tax-aware mindset is to favor bonds issued with low interest rates (a low “coupon”). Since market yields change, bond prices also change to reflect a new fair rate of return. This means bonds with very low, below-market coupons tend to be priced at attractive discounts to par. The lower a bond’s coupon, the higher the price discount. Through this price discount, a bond’s return becomes more valuable. A bond priced at a discount earns its return not only through its coupon, but (importantly) through the gradual appreciation of its price to par maturity. And the greater the price discount, the greater proportion of the bond’s total return will be generated from the bond’s price appreciation. This price appreciation is counted as a capital gain, which bears substantially more favorable tax treatment than ordinary interest income. In an asset class that sweats over basis points (one-hundredths of a percent), this is a highly valuable nuance for taxable clients. And while this approach produces no difference to the pre-tax results you see on the facing page of this letter, it certainly makes a difference to your bank account and in a few other ways which we will share.

Tax Deferral: Taxes on interest income are paid annually as the income is received, so a traditional, high-coupon bond results in a higher tax bill every year. By contrast, a low-coupon, discounted bond gradually moving to par incurs little tax until the year of its sale (or its maturity), effectively postponing much of the tax impact, better compounding an investment’s value.

Success-Based Taxes: Taxes on capital gains are owed only if the bond is sold at a profit. When the bulk of an investment’s expected return comes from price appreciation, this is advantageous. Capital gains tax is, by definition, contingent on the success of the investment. On the other hand, high-coupon bonds generate taxable interest every year, even if the bond later loses value or – even worse – the company goes bankrupt.

Safer Return Generation: Since higher yields typically mean higher credit risk, we are always seeking more conservative ways to achieve safer after-tax returns. By taking advantage of the tax benefits of discounted, low-coupon bonds, we can often match the after-tax return of a higher-yield, higher-risk bond, through a substantially lower-risk company.

Pleasant Surprises: Another benefit comes from company takeovers. Each year, it’s not unusual for four to five percent of public companies to be delisted due to mergers or acquisitions. When this happens, their bonds are very often paid off at par or better. Discounted bonds, in these cases, contain a “hidden bonus” - the chance for an immediate and positive jump in value if such an event occurs. We should add that this value is not theoretical – we experienced two of these events in the portfolio just last year.

Where Flexibility Counts

While this concept is simple, we have taken it very seriously. We have applied this lens as we’ve scoured the market for opportunities. Fortunately, we found an excellent base for tax-advantaged idea generation: the US convertible bond market. These bonds (which must be paid in cash at their maturity unlike their Canadian counterparts) typically bear coupons between zero and two percent and have five-year terms. This US$300 billion-dollar market trades primarily over equity or equity derivative desks, putting it outside the scope of convenience for traditional fixed income investors. We also like that, given the number of issuers (~500), at any given time there are convertible bond issuers that are amid some adversity or mispricing. We have shared convertible bond case studies to highlight this attractive space in prior communications. In sum, our activity in this fixed income market niche is an excellent example of how we use our flexible mandate to generate quality risk-adjusted returns.

So why doesn’t everyone else focus on low coupon bonds? The reasons are many.

Clients: The investment management industry – fixed income in particular - has very substantial customers in pensions, endowments and foundations. These entities are the often the largest and most popular organizations to service. These entities are tax-exempt, so they do not care about the sources of return. Investment managers who count these entities as large clients (almost any manager of scale) may naturally jettison tax considerations as well.

Marketing: Because of the multi-faceted nature of taxes and varying individual tax rates, it is not particularly easy to communicate results with respect to tax. In addition, since pre-tax returns are the industry standard basis of competition, it should not be a surprise that many managers simply optimize for ‘headline’ (pre-tax) fund returns.

Size: For large asset managers (which most fixed income managers are), capital is always required to be put to work. This often presents a problem, where a manager is very much constrained by what’s available in the market. What is available isn’t always economically convenient. Indeed, there are numerous examples of highly liquid bonds in the market having average (or worse) tax characteristics.

Fortunately, we are largely free (or unbothered by) these constraints and have taken full advantage of this for you. If you are interested in your individual mix of taxable gains, we would be delighted to connect on this.

Outlook

It has taken a wholesale change in fiscal, foreign and trade policies, but fixed income is once again pricing in a good portion of the uncertainty many feel about the future. As of this writing, while not at extreme levels, the market has moved to the pessimistic side of the sentiment ledger. This should be welcomed; the more pessimism that is reflected in a bond’s price, the safer an investment it tends to become.

With this recent change in overall attractiveness of the bond market, we have been active in taking advantage of better expected returns in the market, boosting the portfolio’s overall yield through the reduction of hedges and the addition of new credits in the fund. Despite this activity, our positioning remains ‘below market’ in terms of credit risk. Plenty of sand, wrenches and all-caps tweets have been thrown into the gears of the world economy. Perhaps we have already seen “peak uncertainty”, but it also remains to be seen whether we are past “peak pain”. It is impossible to know. This is why we regularly remind ourselves that the only job of economic or market forecasting is to make astrology look respectable. In contrast, our job is simple: find great opportunities come rain or shine, one investment at a time.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg USCorporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these arewidely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investmentmandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks andindices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Funddoes not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and theFund portfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source for datareferenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2025.

Fellow Limited Partners,

In the first quarter of 2025, the Flexible Fixed Income Fund returned +1.3%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and +1.6%,respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.0%, meeting our long-term net return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

While it is easy to expect the world and markets to unfold in a straightforward progression, on occasion, reality brings something different. This year certainly has - from non-linear policy changes to non-linear market reactions.

The Yield is High Again

A defenestration of long-held economic and state doctrine by current US leadership has marked the beginning of something valuable: higher yields. 2025 (and 2026 for that matter) may turn out to be one of the most opportunity-rich years we have seen in a long time. Of course, we do not know for certain if these years will be high returning, but what we do know is that when uncertainty reigns, returns tend to follow, especially in high yield bonds.

In the corporate bond market, two important things have happened. First, in the United States, interest rates for US Treasury bonds have risen substantially on questions regarding the safe-haven status of US assets. This is not a welcome development for US policymakers and might be a step-change that produces a long-term tailwind for fixed income returns. Second, there has been a spike in credit spreads in anticipation of a more difficult economic environment ahead. These two factors have combined to push high yield bond yields back to levels that reflect emerging concerns of recession. This makes the opportunity set more interesting, not less. We are looking forward to the year ahead.

Timely Tax Takeaways

As tax season is upon us, you might welcome something positive on this topic. As the substantial majority of our investors are tax-paying individuals and families, we believe it is our duty to incorporate an after-tax mindset in our bond investment activity. To our delight, we have observed that the market largely does not differentiate between bonds based on their tax characteristics. Naturally, we have been capitalizing on this dynamic for you since the Fund’s inception, more than nine years ago.

The essence of this tax-aware mindset is to favor bonds issued with low interest rates (a low “coupon”). Since market yields change, bond prices also change to reflect a new fair rate of return. This means bonds with very low, below-market coupons tend to be priced at attractive discounts to par. The lower a bond’s coupon, the higher the price discount. Through this price discount, a bond’s return becomes more valuable. A bond priced at a discount earns its return not only through its coupon, but (importantly) through the gradual appreciation of its price to par maturity. And the greater the price discount, the greater proportion of the bond’s total return will be generated from the bond’s price appreciation. This price appreciation is counted as a capital gain, which bears substantially more favorable tax treatment than ordinary interest income. In an asset class that sweats over basis points (one-hundredths of a percent), this is a highly valuable nuance for taxable clients. And while this approach produces no difference to the pre-tax results you see on the facing page of this letter, it certainly makes a difference to your bank account and in a few other ways which we will share.

Tax Deferral: Taxes on interest income are paid annually as the income is received, so a traditional, high-coupon bond results in a higher tax bill every year. By contrast, a low-coupon, discounted bond gradually moving to par incurs little tax until the year of its sale (or its maturity), effectively postponing much of the tax impact, better compounding an investment’s value.

Success-Based Taxes: Taxes on capital gains are owed only if the bond is sold at a profit. When the bulk of an investment’s expected return comes from price appreciation, this is advantageous. Capital gains tax is, by definition, contingent on the success of the investment. On the other hand, high-coupon bonds generate taxable interest every year, even if the bond later loses value or – even worse – the company goes bankrupt.

Safer Return Generation: Since higher yields typically mean higher credit risk, we are always seeking more conservative ways to achieve safer after-tax returns. By taking advantage of the tax benefits of discounted, low-coupon bonds, we can often match the after-tax return of a higher-yield, higher-risk bond, through a substantially lower-risk company.

Pleasant Surprises: Another benefit comes from company takeovers. Each year, it’s not unusual for four to five percent of public companies to be delisted due to mergers or acquisitions. When this happens, their bonds are very often paid off at par or better. Discounted bonds, in these cases, contain a “hidden bonus” - the chance for an immediate and positive jump in value if such an event occurs. We should add that this value is not theoretical – we experienced two of these events in the portfolio just last year.

Where Flexibility Counts

While this concept is simple, we have taken it very seriously. We have applied this lens as we’ve scoured the market for opportunities. Fortunately, we found an excellent base for tax-advantaged idea generation: the US convertible bond market. These bonds (which must be paid in cash at their maturity unlike their Canadian counterparts) typically bear coupons between zero and two percent and have five-year terms. This US$300 billion-dollar market trades primarily over equity or equity derivative desks, putting it outside the scope of convenience for traditional fixed income investors. We also like that, given the number of issuers (~500), at any given time there are convertible bond issuers that are amid some adversity or mispricing. We have shared convertible bond case studies to highlight this attractive space in prior communications. In sum, our activity in this fixed income market niche is an excellent example of how we use our flexible mandate to generate quality risk-adjusted returns.

So why doesn’t everyone else focus on low coupon bonds? The reasons are many.

Clients: The investment management industry – fixed income in particular - has very substantial customers in pensions, endowments and foundations. These entities are the often the largest and most popular organizations to service. These entities are tax-exempt, so they do not care about the sources of return. Investment managers who count these entities as large clients (almost any manager of scale) may naturally jettison tax considerations as well.

Marketing: Because of the multi-faceted nature of taxes and varying individual tax rates, it is not particularly easy to communicate results with respect to tax. In addition, since pre-tax returns are the industry standard basis of competition, it should not be a surprise that many managers simply optimize for ‘headline’ (pre-tax) fund returns.

Size: For large asset managers (which most fixed income managers are), capital is always required to be put to work. This often presents a problem, where a manager is very much constrained by what’s available in the market. What is available isn’t always economically convenient. Indeed, there are numerous examples of highly liquid bonds in the market having average (or worse) tax characteristics.

Fortunately, we are largely free (or unbothered by) these constraints and have taken full advantage of this for you. If you are interested in your individual mix of taxable gains, we would be delighted to connect on this.

Outlook

It has taken a wholesale change in fiscal, foreign and trade policies, but fixed income is once again pricing in a good portion of the uncertainty many feel about the future. As of this writing, while not at extreme levels, the market has moved to the pessimistic side of the sentiment ledger. This should be welcomed; the more pessimism that is reflected in a bond’s price, the safer an investment it tends to become.

With this recent change in overall attractiveness of the bond market, we have been active in taking advantage of better expected returns in the market, boosting the portfolio’s overall yield through the reduction of hedges and the addition of new credits in the fund. Despite this activity, our positioning remains ‘below market’ in terms of credit risk. Plenty of sand, wrenches and all-caps tweets have been thrown into the gears of the world economy. Perhaps we have already seen “peak uncertainty”, but it also remains to be seen whether we are past “peak pain”. It is impossible to know. This is why we regularly remind ourselves that the only job of economic or market forecasting is to make astrology look respectable. In contrast, our job is simple: find great opportunities come rain or shine, one investment at a time.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg USCorporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these arewidely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investmentmandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks andindices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Funddoes not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and theFund portfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source for datareferenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2025.

Fellow Limited Partners,

In the first quarter of 2025, the Flexible Fixed Income Fund returned +1.3%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +0.8% and +1.6%,respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.0%, meeting our long-term net return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

While it is easy to expect the world and markets to unfold in a straightforward progression, on occasion, reality brings something different. This year certainly has - from non-linear policy changes to non-linear market reactions.

The Yield is High Again

A defenestration of long-held economic and state doctrine by current US leadership has marked the beginning of something valuable: higher yields. 2025 (and 2026 for that matter) may turn out to be one of the most opportunity-rich years we have seen in a long time. Of course, we do not know for certain if these years will be high returning, but what we do know is that when uncertainty reigns, returns tend to follow, especially in high yield bonds.

In the corporate bond market, two important things have happened. First, in the United States, interest rates for US Treasury bonds have risen substantially on questions regarding the safe-haven status of US assets. This is not a welcome development for US policymakers and might be a step-change that produces a long-term tailwind for fixed income returns. Second, there has been a spike in credit spreads in anticipation of a more difficult economic environment ahead. These two factors have combined to push high yield bond yields back to levels that reflect emerging concerns of recession. This makes the opportunity set more interesting, not less. We are looking forward to the year ahead.

Timely Tax Takeaways

As tax season is upon us, you might welcome something positive on this topic. As the substantial majority of our investors are tax-paying individuals and families, we believe it is our duty to incorporate an after-tax mindset in our bond investment activity. To our delight, we have observed that the market largely does not differentiate between bonds based on their tax characteristics. Naturally, we have been capitalizing on this dynamic for you since the Fund’s inception, more than nine years ago.

The essence of this tax-aware mindset is to favor bonds issued with low interest rates (a low “coupon”). Since market yields change, bond prices also change to reflect a new fair rate of return. This means bonds with very low, below-market coupons tend to be priced at attractive discounts to par. The lower a bond’s coupon, the higher the price discount. Through this price discount, a bond’s return becomes more valuable. A bond priced at a discount earns its return not only through its coupon, but (importantly) through the gradual appreciation of its price to par maturity. And the greater the price discount, the greater proportion of the bond’s total return will be generated from the bond’s price appreciation. This price appreciation is counted as a capital gain, which bears substantially more favorable tax treatment than ordinary interest income. In an asset class that sweats over basis points (one-hundredths of a percent), this is a highly valuable nuance for taxable clients. And while this approach produces no difference to the pre-tax results you see on the facing page of this letter, it certainly makes a difference to your bank account and in a few other ways which we will share.

Tax Deferral: Taxes on interest income are paid annually as the income is received, so a traditional, high-coupon bond results in a higher tax bill every year. By contrast, a low-coupon, discounted bond gradually moving to par incurs little tax until the year of its sale (or its maturity), effectively postponing much of the tax impact, better compounding an investment’s value.

Success-Based Taxes: Taxes on capital gains are owed only if the bond is sold at a profit. When the bulk of an investment’s expected return comes from price appreciation, this is advantageous. Capital gains tax is, by definition, contingent on the success of the investment. On the other hand, high-coupon bonds generate taxable interest every year, even if the bond later loses value or – even worse – the company goes bankrupt.

Safer Return Generation: Since higher yields typically mean higher credit risk, we are always seeking more conservative ways to achieve safer after-tax returns. By taking advantage of the tax benefits of discounted, low-coupon bonds, we can often match the after-tax return of a higher-yield, higher-risk bond, through a substantially lower-risk company.

Pleasant Surprises: Another benefit comes from company takeovers. Each year, it’s not unusual for four to five percent of public companies to be delisted due to mergers or acquisitions. When this happens, their bonds are very often paid off at par or better. Discounted bonds, in these cases, contain a “hidden bonus” - the chance for an immediate and positive jump in value if such an event occurs. We should add that this value is not theoretical – we experienced two of these events in the portfolio just last year.

Where Flexibility Counts

While this concept is simple, we have taken it very seriously. We have applied this lens as we’ve scoured the market for opportunities. Fortunately, we found an excellent base for tax-advantaged idea generation: the US convertible bond market. These bonds (which must be paid in cash at their maturity unlike their Canadian counterparts) typically bear coupons between zero and two percent and have five-year terms. This US$300 billion-dollar market trades primarily over equity or equity derivative desks, putting it outside the scope of convenience for traditional fixed income investors. We also like that, given the number of issuers (~500), at any given time there are convertible bond issuers that are amid some adversity or mispricing. We have shared convertible bond case studies to highlight this attractive space in prior communications. In sum, our activity in this fixed income market niche is an excellent example of how we use our flexible mandate to generate quality risk-adjusted returns.

So why doesn’t everyone else focus on low coupon bonds? The reasons are many.

Clients: The investment management industry – fixed income in particular - has very substantial customers in pensions, endowments and foundations. These entities are the often the largest and most popular organizations to service. These entities are tax-exempt, so they do not care about the sources of return. Investment managers who count these entities as large clients (almost any manager of scale) may naturally jettison tax considerations as well.

Marketing: Because of the multi-faceted nature of taxes and varying individual tax rates, it is not particularly easy to communicate results with respect to tax. In addition, since pre-tax returns are the industry standard basis of competition, it should not be a surprise that many managers simply optimize for ‘headline’ (pre-tax) fund returns.

Size: For large asset managers (which most fixed income managers are), capital is always required to be put to work. This often presents a problem, where a manager is very much constrained by what’s available in the market. What is available isn’t always economically convenient. Indeed, there are numerous examples of highly liquid bonds in the market having average (or worse) tax characteristics.

Fortunately, we are largely free (or unbothered by) these constraints and have taken full advantage of this for you. If you are interested in your individual mix of taxable gains, we would be delighted to connect on this.

Outlook

It has taken a wholesale change in fiscal, foreign and trade policies, but fixed income is once again pricing in a good portion of the uncertainty many feel about the future. As of this writing, while not at extreme levels, the market has moved to the pessimistic side of the sentiment ledger. This should be welcomed; the more pessimism that is reflected in a bond’s price, the safer an investment it tends to become.

With this recent change in overall attractiveness of the bond market, we have been active in taking advantage of better expected returns in the market, boosting the portfolio’s overall yield through the reduction of hedges and the addition of new credits in the fund. Despite this activity, our positioning remains ‘below market’ in terms of credit risk. Plenty of sand, wrenches and all-caps tweets have been thrown into the gears of the world economy. Perhaps we have already seen “peak uncertainty”, but it also remains to be seen whether we are past “peak pain”. It is impossible to know. This is why we regularly remind ourselves that the only job of economic or market forecasting is to make astrology look respectable. In contrast, our job is simple: find great opportunities come rain or shine, one investment at a time.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect ClassP - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged),iShares Canadian Corporate Bond Index ETF, Bloomberg US High Yield Corporate Bond Index Yield and Bloomberg USCorporate Bond Index Yield as benchmark indices/data for the high yield and corporate bond markets, as these arewidely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investmentmandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks andindices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Funddoes not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and theFund portfolio may contain, among other things, options, short positions and other securities, concentrated levels ofsecurities and may employ leverage not found in these indices. As a result, no market indices are directly comparableto the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute anoffer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are onlyavailable to investors who meet investor suitability and sophistication requirements. While information prepared inthis report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to thecompleteness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for publicuse or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All informationprovided is for informational purposes only and should not be construed as personal investment advice. Users ofthese materials are advised to conduct their own analysis prior to making any investment decision. Source for datareferenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2025.

2025 Q2 Letter

Fellow Limited Partners,

In the second quarter of 2025, the Flexible Fixed Income Fund returned +1.3%. This return compares to our publicly traded high yield and investment grade benchmarks, which returned +3.3% and +0.6%, respectively.

Since its inception in early 2016, the Fund has delivered a compound annual return of 6.0%, meeting our long-term net return expectations of 5% to 7% and exceeding our benchmarks by a meaningful margin.

Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of June 30, 2025. Inception date of the Fund is February 1, 2016. U.S. High Yield Bonds are represented by the iShares U.S. High Yield Bond Index ETF (CAD-Hedged). CanadianInvestment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF

Bond and stock markets began the quarter with a politically-induced faceplant. While generally unpleasant, this was welcome to us as yields climbed across the entire fixed income market. Amidst both the volatility and through the remainder of the quarter, we took the opportunity to further shape the portfolio by monetizing hedges and mature ideas while entering new positions with high promise. The second quarter was one of our most active in years.

Extremes, Entries and Exits

Every few years, the market moves to optimistic extremes in pricing where the extra yield a bond carries does not compensate for its risk. We took advantage of this in 2018 by shorting long term corporate bonds and buying their long-term government benchmarks. We took advantage of this again in 2021, once the central bank induced rally in credit appeared to be in its twilight. And once the market moved back to an extreme in late 2024, we took advantage of this dynamic once again. The hedge’s presence in the portfolio, while not observable in April’s monthly return, was very evident early in the month, where the portfolio was roughly flat (based on Bloomberg BVAL pricing), while our high yield benchmark was down nearly 4 percent. While this hedge was not responsible for all of the capital preservation in the portfolio, it was a top contributor. As we had made solid profits on this hedge with credit spreads widening meaningfully toward our target, we opted to exit about 30% of this hedge.

Switching Convertibles

In 2022, we bought numerous convertible bonds trading at extraordinary discounts. At its zenith, about 70% of the portfolio was comprised of convertible bonds. Almost all of these bonds had substantial market cap cushions and cash balances. At the same time, the capital strategy of these issuers was rapidly swinging credit-friendly. It was an excellent setup. Fast forward three years, most of these bonds have evolved into quite conservative, short-term credits, which held up exceptionally well in April. The reality is, however, that while risk is exceptionally low in these investments, bonds due in a year don’t tend to contain much upside potential either. While the credit market itself is very richly valued, we have found opportunities in rotating out of fully-priced ideas that have played out into a particular kind of situation we favor: ones with what we believe contain unrecognized price appreciation on account of the engaged principals involved at these issuers.

The Power of Principals

A hallmark of fixed income investing is letting time pass in exchange for income. Investors, through the terms of their debt contract are “paid to wait”. But just like a mortgage sometimes comes to an early end when the underlying real estate asset changes hands or is otherwise restructured, extraordinary events can pose distinct, value-generative opportunities for certain bonds. Quite crucially, these events tend to be driven socially through decisions and influence of corporate directors. Occasionally, these directors happen to be large owners of a company. We appreciate these situations as they tend to be rich in opportunity from a bond perspective. In addition, since we are ‘paid to wait’ as a bond investor, the character of our investment affords us to be patient with the arrival of shareholder engagement and extraordinary bondholder value creation. Since we are paid to wait, our preference is to use our skill in identifying opportunities ripe for this kind of activity before it happens to gain upside potential that is often not yet foreseen by the credit market. In these situations, we believe we are picking up loonies for 80 and 90 cents. To show you what we mean in practice, we’ll provide three cases, all of which had significant developments in 2025.

Victoria’s Secret

We have long been a debt investor in Victoria’s Secret, dating back to its existence within the L Brands parent company. After having exited many years earlier, we found the situation became more interesting following its governance overhaul and the split of L Brands into Victoria’s Secret (VSCO) and Bath and Body Works in 2021. As a quite modestly levered credit, in our view, VSCO had been overly punished relative to its fundamentals, as the bonds traded down through 2022 and 2023. This credit on its own was fairly attractive, but we thought two other factors made the situation particularly compelling: timing and ownership. From a timing perspective, the typical two-year restriction on a corporate sale following a spinoff had just expired for VSCO, making this valuable brand potentially a ‘free agent’ on the market. From an ownership perspective, Windacre Partnership and BBRC International (BBRC) had become new shareholders following its spin. In understanding Windacre’s portfolio concentration and its engagement with Nielsen’s take-private, it was clear that Windacre was not an ordinary shareholder. In addition, BBRC’s involvement—ostensibly the investment office of Brett Blundy—was remarkable as well, as his position topped 10% of the company. An Australian billionaire with expertise in retail, Blundy has been instrumental in the growth and sale of not one, but two, lingerie brands. Given BBRC's balance sheet, domain expertise and transactional history, we became quite optimistic on the value of the seemingly discarded bonds offered in the market. We bought VSCO’s 2029 bonds in August of 2023 in the low 70’s with a yield of greater than 10%. Fast forward to Q2 2025, BBRC has flipped from a passive to an active filer and publicly challenged the company in June. The bonds today have appreciated significantly to around 93.

Sitting with a gain of about 20 points (not to mention the annual 4.625 points of income), it turned out that we were well-paid to wait for BBRC to take a firmer position on the company and its board.

Rapid7 Inc

Our first investment in Rapid7 dates back also to October of 2023, where we entered its convertible bonds due 2027 at 87.125. At this time, we liked the credit as the company was well-capitalized and had an increasingly credit-friendly capital strategy, focused on free cash flow generation. But what made the situation more interesting was spotting a Reuters report, citing takeover interest in the company earlier in the year—notably from private equity. When private equity purchases companies, it is for cash. Therefore, the convertible bonds in that case would see a ~13 point lift to par—an option that the market did not appear to be ascribing much value to. Between its value and optionality, we bought a modest starter position. What made things more interesting, however, is that at least two dealers were holding meaningful stock on swap for their clients—a form of ownership often used by a particular kind of investor: activists. As we continued to build our position, we were not surprised to see activists surface in the second half of 2024—in this case on the part of Jana Partners and Cannae Holdings. Fast forward to Q2 2025, the company has settled a co-operation agreement with Jana that appoints three new directors to the board. Today, the bonds have earned returns in a tax-efficient manner, moving gradually into the low 90’s, and today still containing reasonable upside to par on a potential take-private event.

Trimas Corp

Quite often we will take interest in a situation, but find ourselves on the sideline until some threshold event changes the situation. We had started paying attention to Trimas on the back of Barington Capital’s public engagement with the company in 2023. Although it was a high-quality (BB-rated) high yield issuer, the company delivered a low-quality equity investment result since its public debut in 2021. In December of 2023, Barington press released a very reasonable case for value maximization at Trimas. Unfortunately, company leadership appeared to show little receptivity. That is, until an investor showed up. This investor was Trend International AG, which filed a 13-D in October of 2024, with ownership of more than 10% of the company (vs Barington’s position of less than 2%). As we were learning that the investor behind Trend International was a private, accomplished consumer packaging entrepreneur, something happened on January 6th that took us off the sidelines. On this day, Trimas announced a transition plan for its President & CEO Thomas Amato. By our interpretation, its engaged shareholders were finally gaining traction. Soon after this news, we bought its 4.125% senior notes due 2028 at 91.875 for a yield of 6.3%.

Fast forward to Q2 2025, the company’s welcomed this entrepreneur to its board and has also found itself with a second activist in its shareholder registry: Irenic Capital Management led by Adam Katz who has deep expertise in aerospace investing from his time at Elliott Management. Year-to-date, Trimas equity is up about 50%, suggesting confidence in the value unlock driven by its principals, while the bonds have moved in the same direction, outpacing the market, delivering an IRR in the teens since our purchase.

Outlook

The beginning of the third quarter has marked a notable tightening in credit spreads. With this recent move tighter, the additional yield investors collect has reached an extreme low. But we see this as an opportunity on two fronts: Firstly, credit spreads themselves are highly effective to use as a hedge against volatile markets. We have capitalized on conditions like these before, setting hedges in 2018 and 2021. To us, it is much akin to owning a mispriced fire insurance policy in California. The price is simply wrong relative to the frequency and severity of risk. We are positioned with a hedge currently comprising 45% of the Fund. Secondly, a reality of the market is when the credit market is wide open like it is today, more deals tend to happen. This also means that activist shareholders who are looking to drive a corporate sale are more likely to succeed. This, too, should bode well for our approach and our portfolio as we move through the remainder of 2025.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

*All market data referenced sourced from Bloomberg LP*

Schedule a

Conversation

Connect with Peers

Explore Our Full Library

Library

Minimizing Tax Drag (Part 2)