Fellow Limited Partners,

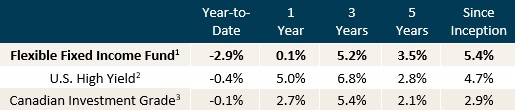

In the first quarter of 2026, the Flexible Fixed Income Fund returned -2.89%.1 This return compares to our publicly traded high yield and investment grade benchmarks, which returned -0.4%2 and -0.1%,3 respectively.

Since its inception in early 2016, the Fund has delivered a compound annual net return of 5.4%, meeting our long-term net return expectations of 5% to 7% and exceeding both of our benchmarks.

Performance

In one of the most geopolitically eventful quarters we’ve seen in decades, it was not a surprise to see uneven performance across sectors and asset classes. The dominant theme since 2022 - the AI wrecking ball - continued to smash its way through the market, colliding with its newest victim - the software sector. On the public side, many software stocks and credits, took a pronounced hit in Q1. On the private side, a crescendo of concern in the direct lending and syndicated loan market continued to build as record-high redemption requests were announced across an array of funds.

While we were early in reducing the portfolio's exposure to the tech sector since last year, a repricing in this space detracted from Fund returns in the first quarter. In the context of Q1 tech activity, we exited one cybersecurity credit where we believed the risk/reward was no longer attractive and we added an equity hedge to another health-tech credit as more efficient way to reduce investment risk in the position. While the sector has faced headwinds, we believe the resulting reset in valuations creates compelling opportunities, particularly in higher quality credits, where we continue to see solid credit fundamentals now at higher yields.

The ‘SaaSpocalypse’

The software sector has rewarded its investors handsomely for decades. Some marquee private equity franchises have even been built around software. Public market investors have seen similar success across cap ranges, with the largest cap holdings being standout performers. Between the performance of the stocks themselves and the economics of the underlying businesses, the space has been arguably ‘easy to own’, attracting substantial capital and extended equity valuations.

That is, until the Claude Code moment - the moment in February 2025 when software investors began running for the exits.

With equity valuations of software companies crashing down since, investor concerns spread to the private credit space, and for good reason. Private credit had been a sector that financed deals at high single digit or even double-digit leverage multiples on the simple basis of the “loan-to-value” of the deal. This approach becomes obviously problematic when the market cost of capital of an 8x levered deal goes into the teens. The valuation extremes in software deals since 2021 have set up many situations in the market where a refinancing is set to ruin the go-forward economics of the company’s owner.

What We’ve Done in SaaS

On the back of declines in technology equity and bond valuations in 2022, we made opportunistic investments in a variety of convertible bonds backed by quality companies with large cash balances trading at 60 to 80 cents on the dollar. The majority of these investments were in bonds with maturity dates in the 2025 to 2027 range. Having exited many of these investments in 2025 at attractive gains, our risk exposure within the software space declined and we narrowed our issuer composition. While we maintain still above-average exposure to the technology sector, we’ve offset this exposure through issuer selection where we own issuers of high credit quality, relatively short terms and, in many cases, undervalued takeout optionality.

Below shows our core unhedged positions in the technology sector, which totals 23% of the portfolio as of this writing. Given the quality of these credits, the terms of the securities, at current prices we see the risk-reward of this pocket to be excellent.

Bandwidth is a company we have previously featured at length. Bandwidth provides its customers software to connect to its telephone network. The company’s software is a “tool” able to be used by both people and voice AI agents. Given this fact, in our view, Bandwidth is positioned to be a big AI winner as the agentic ecosystem expands to voice communications over the mid-to-long term. In the meantime, Bandwidth is forecasting an acceleration of top line growth (+16%) and profitability (26e EBITDA +29%) due to its expanding presence in the “Global 2000” enterprise market.4 We see ample fundamental and technical downside protection in the bonds as the company’s implied 2026 free cash flow exceeds $90mm (vs $150mm 28’s left).4,5 In Q1,Bandwidth paid down $100mm of its 2028 bond issue, demonstrating a genuine commitment to a conservative capital structure.5

Five9 provides cloud contact center software for organizations that want a turnkey tech stack for customer experience (sales + support). Despite Five9 being in the AI battleground, we find its bonds attractive regardless for many reasons: 1) its cash balance today nearly covers all of its debt obligations; 2) the company expects to see its business and profitability grow at a high single digit pace in 2026;6 3) the company publicly acknowledged it received a takeover approach (likely by Zoom - a $27Bn market cap and 8.4x 26e EBITDA vs FIVN’s 1.2Bn and 4.2x); 4) an activist investor who was publicly pushing for a sale of the company is now on Five9’s board;7 5) the sizeable discount to par (86.5 price) and solid upside (+15.6% to a par change of control put) in the event of a deal; and 6) FIVN’s ample free cash flow generation which should allow it to maintain its very low net debt position, even in the event of share buybacks or acquisitions.

Blackline provides mission critical enterprise accounting software to the office of the CFO. Blackline’s core software offering is a well-established solution used for financial closes - enabling its users to stitch together information from differing types of accounting software into a coherent end-of-quarter financial close for the parent, with auditable logs all way up the chain and through time. With a balance sheet that is also nearly net-debt free, the company’s credit risk is very low, while the structure of its convertible bonds offers equity upside potential in the event of a takeover. On this note, less than a year ago, SAP privately offered to buy Blackline for $669 - a bid the company ostensibly dismissed. Today, Blackline equity trades in the low 30’s.10 As activist pressure rose in the market, Engaged Capital took a leadership role and has won the appointment of two directors to the company’s board, marking a material shift in power away from its founder and towards its shareholders - many of which have publicly called on Blackline’s board to engage with SAP.

Constellation Software is a well-followed serial acquirer of niche “vertical market” software businesses. We have owned its floating rate debentures since 2016 and see attractive risk adjusted value in its debenture, which has a coupon that resets every year at Statistics Canada All-Items CPI (YoY change) plus 6.5%. Based on today’s prices and assuming 2% long term inflation, we see this security carrying an implied 6.8% internal rate of return. If this was not attractive enough, the debenture also contains a put option at 100 cents on the dollar, further reducing investment risk. Considering the company’s exceptionally low credit risk (CSI is investment grade rated), we believe this obscure, TSX-listed security is a hidden gem in the Canadian market.

Outlook

The geopolitical and market volatility of the first quarter of 2026 has reminded us the importance of respecting uncertainty; that we need to acknowledge a broad range of future scenarios when we make an investment. This is why we remain focused on the micro. The investments detailed above serve as examples within out-of-favour spaces, built around credits where the downside is bounded by cash balances, high credit quality and a fixed maturity date.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Footnotes:

1 Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of March 31,2026. Inception date of the Fund is February 1, 2016.

2 U.S. High Yield Bonds are represented by theiShares U.S. High Yield Bond Index ETF (CAD-Hedged). See Additional Disclosures below.

3 Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures below.

4. Bandwidth Inc Q4 and Year-ended 2025 Earnings Presentation

5 Bandwidth Inc Press Release (3/2026)

6 Five9 Q4 and Year-ended 2025 Presentation

7 Reuters– July 16, 2024; Co-operationagreement 8-K

8 BlackLineQ4 and Year-ended 2025 Results

9 Exclusive:Germany's SAP mulls new bid for software firm BlackLine, source says.

10 Bloomberg

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged) (TSX: XHY) and the iShares Canadian Corporate Bond Index ETF (TSX: XCB) as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2026.

Fellow Limited Partners,

In the first quarter of 2026, the Flexible Fixed Income Fund returned -2.89%.1 This return compares to our publicly traded high yield and investment grade benchmarks, which returned -0.4%2 and -0.1%,3 respectively.

Since its inception in early 2016, the Fund has delivered a compound annual net return of 5.4%, meeting our long-term net return expectations of 5% to 7% and exceeding both of our benchmarks.

Performance

In one of the most geopolitically eventful quarters we’ve seen in decades, it was not a surprise to see uneven performance across sectors and asset classes. The dominant theme since 2022 - the AI wrecking ball - continued to smash its way through the market, colliding with its newest victim - the software sector. On the public side, many software stocks and credits, took a pronounced hit in Q1. On the private side, a crescendo of concern in the direct lending and syndicated loan market continued to build as record-high redemption requests were announced across an array of funds.

While we were early in reducing the portfolio's exposure to the tech sector since last year, a repricing in this space detracted from Fund returns in the first quarter. In the context of Q1 tech activity, we exited one cybersecurity credit where we believed the risk/reward was no longer attractive and we added an equity hedge to another health-tech credit as more efficient way to reduce investment risk in the position. While the sector has faced headwinds, we believe the resulting reset in valuations creates compelling opportunities, particularly in higher quality credits, where we continue to see solid credit fundamentals now at higher yields.

The ‘SaaSpocalypse’

The software sector has rewarded its investors handsomely for decades. Some marquee private equity franchises have even been built around software. Public market investors have seen similar success across cap ranges, with the largest cap holdings being standout performers. Between the performance of the stocks themselves and the economics of the underlying businesses, the space has been arguably ‘easy to own’, attracting substantial capital and extended equity valuations.

That is, until the Claude Code moment - the moment in February 2025 when software investors began running for the exits.

With equity valuations of software companies crashing down since, investor concerns spread to the private credit space, and for good reason. Private credit had been a sector that financed deals at high single digit or even double-digit leverage multiples on the simple basis of the “loan-to-value” of the deal. This approach becomes obviously problematic when the market cost of capital of an 8x levered deal goes into the teens. The valuation extremes in software deals since 2021 have set up many situations in the market where a refinancing is set to ruin the go-forward economics of the company’s owner.

What We’ve Done in SaaS

On the back of declines in technology equity and bond valuations in 2022, we made opportunistic investments in a variety of convertible bonds backed by quality companies with large cash balances trading at 60 to 80 cents on the dollar. The majority of these investments were in bonds with maturity dates in the 2025 to 2027 range. Having exited many of these investments in 2025 at attractive gains, our risk exposure within the software space declined and we narrowed our issuer composition. While we maintain still above-average exposure to the technology sector, we’ve offset this exposure through issuer selection where we own issuers of high credit quality, relatively short terms and, in many cases, undervalued takeout optionality.

Below shows our core unhedged positions in the technology sector, which totals 23% of the portfolio as of this writing. Given the quality of these credits, the terms of the securities, at current prices we see the risk-reward of this pocket to be excellent.

Bandwidth is a company we have previously featured at length. Bandwidth provides its customers software to connect to its telephone network. The company’s software is a “tool” able to be used by both people and voice AI agents. Given this fact, in our view, Bandwidth is positioned to be a big AI winner as the agentic ecosystem expands to voice communications over the mid-to-long term. In the meantime, Bandwidth is forecasting an acceleration of top line growth (+16%) and profitability (26e EBITDA +29%) due to its expanding presence in the “Global 2000” enterprise market.4 We see ample fundamental and technical downside protection in the bonds as the company’s implied 2026 free cash flow exceeds $90mm (vs $150mm 28’s left).4,5 In Q1,Bandwidth paid down $100mm of its 2028 bond issue, demonstrating a genuine commitment to a conservative capital structure.5

Five9 provides cloud contact center software for organizations that want a turnkey tech stack for customer experience (sales + support). Despite Five9 being in the AI battleground, we find its bonds attractive regardless for many reasons: 1) its cash balance today nearly covers all of its debt obligations; 2) the company expects to see its business and profitability grow at a high single digit pace in 2026;6 3) the company publicly acknowledged it received a takeover approach (likely by Zoom - a $27Bn market cap and 8.4x 26e EBITDA vs FIVN’s 1.2Bn and 4.2x); 4) an activist investor who was publicly pushing for a sale of the company is now on Five9’s board;7 5) the sizeable discount to par (86.5 price) and solid upside (+15.6% to a par change of control put) in the event of a deal; and 6) FIVN’s ample free cash flow generation which should allow it to maintain its very low net debt position, even in the event of share buybacks or acquisitions.

Blackline provides mission critical enterprise accounting software to the office of the CFO. Blackline’s core software offering is a well-established solution used for financial closes - enabling its users to stitch together information from differing types of accounting software into a coherent end-of-quarter financial close for the parent, with auditable logs all way up the chain and through time. With a balance sheet that is also nearly net-debt free, the company’s credit risk is very low, while the structure of its convertible bonds offers equity upside potential in the event of a takeover. On this note, less than a year ago, SAP privately offered to buy Blackline for $669 - a bid the company ostensibly dismissed. Today, Blackline equity trades in the low 30’s.10 As activist pressure rose in the market, Engaged Capital took a leadership role and has won the appointment of two directors to the company’s board, marking a material shift in power away from its founder and towards its shareholders - many of which have publicly called on Blackline’s board to engage with SAP.

Constellation Software is a well-followed serial acquirer of niche “vertical market” software businesses. We have owned its floating rate debentures since 2016 and see attractive risk adjusted value in its debenture, which has a coupon that resets every year at Statistics Canada All-Items CPI (YoY change) plus 6.5%. Based on today’s prices and assuming 2% long term inflation, we see this security carrying an implied 6.8% internal rate of return. If this was not attractive enough, the debenture also contains a put option at 100 cents on the dollar, further reducing investment risk. Considering the company’s exceptionally low credit risk (CSI is investment grade rated), we believe this obscure, TSX-listed security is a hidden gem in the Canadian market.

Outlook

The geopolitical and market volatility of the first quarter of 2026 has reminded us the importance of respecting uncertainty; that we need to acknowledge a broad range of future scenarios when we make an investment. This is why we remain focused on the micro. The investments detailed above serve as examples within out-of-favour spaces, built around credits where the downside is bounded by cash balances, high credit quality and a fixed maturity date.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Footnotes:

1 Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of March 31,2026. Inception date of the Fund is February 1, 2016.

2 U.S. High Yield Bonds are represented by theiShares U.S. High Yield Bond Index ETF (CAD-Hedged). See Additional Disclosures below.

3 Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures below.

4. Bandwidth Inc Q4 and Year-ended 2025 Earnings Presentation

5 Bandwidth Inc Press Release (3/2026)

6 Five9 Q4 and Year-ended 2025 Presentation

7 Reuters– July 16, 2024; Co-operationagreement 8-K

8 BlackLineQ4 and Year-ended 2025 Results

9 Exclusive:Germany's SAP mulls new bid for software firm BlackLine, source says.

10 Bloomberg

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged) (TSX: XHY) and the iShares Canadian Corporate Bond Index ETF (TSX: XCB) as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2026.

Fellow Limited Partners,

In the first quarter of 2026, the Flexible Fixed Income Fund returned -2.89%.1 This return compares to our publicly traded high yield and investment grade benchmarks, which returned -0.4%2 and -0.1%,3 respectively.

Since its inception in early 2016, the Fund has delivered a compound annual net return of 5.4%, meeting our long-term net return expectations of 5% to 7% and exceeding both of our benchmarks.

Performance

In one of the most geopolitically eventful quarters we’ve seen in decades, it was not a surprise to see uneven performance across sectors and asset classes. The dominant theme since 2022 - the AI wrecking ball - continued to smash its way through the market, colliding with its newest victim - the software sector. On the public side, many software stocks and credits, took a pronounced hit in Q1. On the private side, a crescendo of concern in the direct lending and syndicated loan market continued to build as record-high redemption requests were announced across an array of funds.

While we were early in reducing the portfolio's exposure to the tech sector since last year, a repricing in this space detracted from Fund returns in the first quarter. In the context of Q1 tech activity, we exited one cybersecurity credit where we believed the risk/reward was no longer attractive and we added an equity hedge to another health-tech credit as more efficient way to reduce investment risk in the position. While the sector has faced headwinds, we believe the resulting reset in valuations creates compelling opportunities, particularly in higher quality credits, where we continue to see solid credit fundamentals now at higher yields.

The ‘SaaSpocalypse’

The software sector has rewarded its investors handsomely for decades. Some marquee private equity franchises have even been built around software. Public market investors have seen similar success across cap ranges, with the largest cap holdings being standout performers. Between the performance of the stocks themselves and the economics of the underlying businesses, the space has been arguably ‘easy to own’, attracting substantial capital and extended equity valuations.

That is, until the Claude Code moment - the moment in February 2025 when software investors began running for the exits.

With equity valuations of software companies crashing down since, investor concerns spread to the private credit space, and for good reason. Private credit had been a sector that financed deals at high single digit or even double-digit leverage multiples on the simple basis of the “loan-to-value” of the deal. This approach becomes obviously problematic when the market cost of capital of an 8x levered deal goes into the teens. The valuation extremes in software deals since 2021 have set up many situations in the market where a refinancing is set to ruin the go-forward economics of the company’s owner.

What We’ve Done in SaaS

On the back of declines in technology equity and bond valuations in 2022, we made opportunistic investments in a variety of convertible bonds backed by quality companies with large cash balances trading at 60 to 80 cents on the dollar. The majority of these investments were in bonds with maturity dates in the 2025 to 2027 range. Having exited many of these investments in 2025 at attractive gains, our risk exposure within the software space declined and we narrowed our issuer composition. While we maintain still above-average exposure to the technology sector, we’ve offset this exposure through issuer selection where we own issuers of high credit quality, relatively short terms and, in many cases, undervalued takeout optionality.

Below shows our core unhedged positions in the technology sector, which totals 23% of the portfolio as of this writing. Given the quality of these credits, the terms of the securities, at current prices we see the risk-reward of this pocket to be excellent.

Bandwidth is a company we have previously featured at length. Bandwidth provides its customers software to connect to its telephone network. The company’s software is a “tool” able to be used by both people and voice AI agents. Given this fact, in our view, Bandwidth is positioned to be a big AI winner as the agentic ecosystem expands to voice communications over the mid-to-long term. In the meantime, Bandwidth is forecasting an acceleration of top line growth (+16%) and profitability (26e EBITDA +29%) due to its expanding presence in the “Global 2000” enterprise market.4 We see ample fundamental and technical downside protection in the bonds as the company’s implied 2026 free cash flow exceeds $90mm (vs $150mm 28’s left).4,5 In Q1,Bandwidth paid down $100mm of its 2028 bond issue, demonstrating a genuine commitment to a conservative capital structure.5

Five9 provides cloud contact center software for organizations that want a turnkey tech stack for customer experience (sales + support). Despite Five9 being in the AI battleground, we find its bonds attractive regardless for many reasons: 1) its cash balance today nearly covers all of its debt obligations; 2) the company expects to see its business and profitability grow at a high single digit pace in 2026;6 3) the company publicly acknowledged it received a takeover approach (likely by Zoom - a $27Bn market cap and 8.4x 26e EBITDA vs FIVN’s 1.2Bn and 4.2x); 4) an activist investor who was publicly pushing for a sale of the company is now on Five9’s board;7 5) the sizeable discount to par (86.5 price) and solid upside (+15.6% to a par change of control put) in the event of a deal; and 6) FIVN’s ample free cash flow generation which should allow it to maintain its very low net debt position, even in the event of share buybacks or acquisitions.

Blackline provides mission critical enterprise accounting software to the office of the CFO. Blackline’s core software offering is a well-established solution used for financial closes - enabling its users to stitch together information from differing types of accounting software into a coherent end-of-quarter financial close for the parent, with auditable logs all way up the chain and through time. With a balance sheet that is also nearly net-debt free, the company’s credit risk is very low, while the structure of its convertible bonds offers equity upside potential in the event of a takeover. On this note, less than a year ago, SAP privately offered to buy Blackline for $669 - a bid the company ostensibly dismissed. Today, Blackline equity trades in the low 30’s.10 As activist pressure rose in the market, Engaged Capital took a leadership role and has won the appointment of two directors to the company’s board, marking a material shift in power away from its founder and towards its shareholders - many of which have publicly called on Blackline’s board to engage with SAP.

Constellation Software is a well-followed serial acquirer of niche “vertical market” software businesses. We have owned its floating rate debentures since 2016 and see attractive risk adjusted value in its debenture, which has a coupon that resets every year at Statistics Canada All-Items CPI (YoY change) plus 6.5%. Based on today’s prices and assuming 2% long term inflation, we see this security carrying an implied 6.8% internal rate of return. If this was not attractive enough, the debenture also contains a put option at 100 cents on the dollar, further reducing investment risk. Considering the company’s exceptionally low credit risk (CSI is investment grade rated), we believe this obscure, TSX-listed security is a hidden gem in the Canadian market.

Outlook

The geopolitical and market volatility of the first quarter of 2026 has reminded us the importance of respecting uncertainty; that we need to acknowledge a broad range of future scenarios when we make an investment. This is why we remain focused on the micro. The investments detailed above serve as examples within out-of-favour spaces, built around credits where the downside is bounded by cash balances, high credit quality and a fixed maturity date.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Footnotes:

1 Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of March 31,2026. Inception date of the Fund is February 1, 2016.

2 U.S. High Yield Bonds are represented by theiShares U.S. High Yield Bond Index ETF (CAD-Hedged). See Additional Disclosures below.

3 Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures below.

4. Bandwidth Inc Q4 and Year-ended 2025 Earnings Presentation

5 Bandwidth Inc Press Release (3/2026)

6 Five9 Q4 and Year-ended 2025 Presentation

7 Reuters– July 16, 2024; Co-operationagreement 8-K

8 BlackLineQ4 and Year-ended 2025 Results

9 Exclusive:Germany's SAP mulls new bid for software firm BlackLine, source says.

10 Bloomberg

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged) (TSX: XHY) and the iShares Canadian Corporate Bond Index ETF (TSX: XCB) as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2026.

Fellow Limited Partners,

In the first quarter of 2026, the Flexible Fixed Income Fund returned -2.89%.1 This return compares to our publicly traded high yield and investment grade benchmarks, which returned -0.4%2 and -0.1%,3 respectively.

Since its inception in early 2016, the Fund has delivered a compound annual net return of 5.4%, meeting our long-term net return expectations of 5% to 7% and exceeding both of our benchmarks.

Performance

In one of the most geopolitically eventful quarters we’ve seen in decades, it was not a surprise to see uneven performance across sectors and asset classes. The dominant theme since 2022 - the AI wrecking ball - continued to smash its way through the market, colliding with its newest victim - the software sector. On the public side, many software stocks and credits, took a pronounced hit in Q1. On the private side, a crescendo of concern in the direct lending and syndicated loan market continued to build as record-high redemption requests were announced across an array of funds.

While we were early in reducing the portfolio's exposure to the tech sector since last year, a repricing in this space detracted from Fund returns in the first quarter. In the context of Q1 tech activity, we exited one cybersecurity credit where we believed the risk/reward was no longer attractive and we added an equity hedge to another health-tech credit as more efficient way to reduce investment risk in the position. While the sector has faced headwinds, we believe the resulting reset in valuations creates compelling opportunities, particularly in higher quality credits, where we continue to see solid credit fundamentals now at higher yields.

The ‘SaaSpocalypse’

The software sector has rewarded its investors handsomely for decades. Some marquee private equity franchises have even been built around software. Public market investors have seen similar success across cap ranges, with the largest cap holdings being standout performers. Between the performance of the stocks themselves and the economics of the underlying businesses, the space has been arguably ‘easy to own’, attracting substantial capital and extended equity valuations.

That is, until the Claude Code moment - the moment in February 2025 when software investors began running for the exits.

With equity valuations of software companies crashing down since, investor concerns spread to the private credit space, and for good reason. Private credit had been a sector that financed deals at high single digit or even double-digit leverage multiples on the simple basis of the “loan-to-value” of the deal. This approach becomes obviously problematic when the market cost of capital of an 8x levered deal goes into the teens. The valuation extremes in software deals since 2021 have set up many situations in the market where a refinancing is set to ruin the go-forward economics of the company’s owner.

What We’ve Done in SaaS

On the back of declines in technology equity and bond valuations in 2022, we made opportunistic investments in a variety of convertible bonds backed by quality companies with large cash balances trading at 60 to 80 cents on the dollar. The majority of these investments were in bonds with maturity dates in the 2025 to 2027 range. Having exited many of these investments in 2025 at attractive gains, our risk exposure within the software space declined and we narrowed our issuer composition. While we maintain still above-average exposure to the technology sector, we’ve offset this exposure through issuer selection where we own issuers of high credit quality, relatively short terms and, in many cases, undervalued takeout optionality.

Below shows our core unhedged positions in the technology sector, which totals 23% of the portfolio as of this writing. Given the quality of these credits, the terms of the securities, at current prices we see the risk-reward of this pocket to be excellent.

Bandwidth is a company we have previously featured at length. Bandwidth provides its customers software to connect to its telephone network. The company’s software is a “tool” able to be used by both people and voice AI agents. Given this fact, in our view, Bandwidth is positioned to be a big AI winner as the agentic ecosystem expands to voice communications over the mid-to-long term. In the meantime, Bandwidth is forecasting an acceleration of top line growth (+16%) and profitability (26e EBITDA +29%) due to its expanding presence in the “Global 2000” enterprise market.4 We see ample fundamental and technical downside protection in the bonds as the company’s implied 2026 free cash flow exceeds $90mm (vs $150mm 28’s left).4,5 In Q1,Bandwidth paid down $100mm of its 2028 bond issue, demonstrating a genuine commitment to a conservative capital structure.5

Five9 provides cloud contact center software for organizations that want a turnkey tech stack for customer experience (sales + support). Despite Five9 being in the AI battleground, we find its bonds attractive regardless for many reasons: 1) its cash balance today nearly covers all of its debt obligations; 2) the company expects to see its business and profitability grow at a high single digit pace in 2026;6 3) the company publicly acknowledged it received a takeover approach (likely by Zoom - a $27Bn market cap and 8.4x 26e EBITDA vs FIVN’s 1.2Bn and 4.2x); 4) an activist investor who was publicly pushing for a sale of the company is now on Five9’s board;7 5) the sizeable discount to par (86.5 price) and solid upside (+15.6% to a par change of control put) in the event of a deal; and 6) FIVN’s ample free cash flow generation which should allow it to maintain its very low net debt position, even in the event of share buybacks or acquisitions.

Blackline provides mission critical enterprise accounting software to the office of the CFO. Blackline’s core software offering is a well-established solution used for financial closes - enabling its users to stitch together information from differing types of accounting software into a coherent end-of-quarter financial close for the parent, with auditable logs all way up the chain and through time. With a balance sheet that is also nearly net-debt free, the company’s credit risk is very low, while the structure of its convertible bonds offers equity upside potential in the event of a takeover. On this note, less than a year ago, SAP privately offered to buy Blackline for $669 - a bid the company ostensibly dismissed. Today, Blackline equity trades in the low 30’s.10 As activist pressure rose in the market, Engaged Capital took a leadership role and has won the appointment of two directors to the company’s board, marking a material shift in power away from its founder and towards its shareholders - many of which have publicly called on Blackline’s board to engage with SAP.

Constellation Software is a well-followed serial acquirer of niche “vertical market” software businesses. We have owned its floating rate debentures since 2016 and see attractive risk adjusted value in its debenture, which has a coupon that resets every year at Statistics Canada All-Items CPI (YoY change) plus 6.5%. Based on today’s prices and assuming 2% long term inflation, we see this security carrying an implied 6.8% internal rate of return. If this was not attractive enough, the debenture also contains a put option at 100 cents on the dollar, further reducing investment risk. Considering the company’s exceptionally low credit risk (CSI is investment grade rated), we believe this obscure, TSX-listed security is a hidden gem in the Canadian market.

Outlook

The geopolitical and market volatility of the first quarter of 2026 has reminded us the importance of respecting uncertainty; that we need to acknowledge a broad range of future scenarios when we make an investment. This is why we remain focused on the micro. The investments detailed above serve as examples within out-of-favour spaces, built around credits where the downside is bounded by cash balances, high credit quality and a fixed maturity date.

Thank you for your investment in the Ewing Morris Flexible Fixed Income Fund.

Footnotes:

1 Ewing Morris Flexible Fixed Income Fund LP returns reflect Class P - Master Series, net of fees and expenses as of March 31,2026. Inception date of the Fund is February 1, 2016.

2 U.S. High Yield Bonds are represented by theiShares U.S. High Yield Bond Index ETF (CAD-Hedged). See Additional Disclosures below.

3 Canadian Investment Grade Bonds are represented by the iShares Canadian Corporate Bond Index ETF. See Additional Disclosures below.

4. Bandwidth Inc Q4 and Year-ended 2025 Earnings Presentation

5 Bandwidth Inc Press Release (3/2026)

6 Five9 Q4 and Year-ended 2025 Presentation

7 Reuters– July 16, 2024; Co-operationagreement 8-K

8 BlackLineQ4 and Year-ended 2025 Results

9 Exclusive:Germany's SAP mulls new bid for software firm BlackLine, source says.

10 Bloomberg

Inception date of the Flexible Fixed Income Fund is February 1, 2016. Flexible Fixed Income Fund returns reflect Class P - Master Series, net of fees and expenses. We have listed the iShares U.S. High Yield Bond Index ETF (CAD-Hedged) (TSX: XHY) and the iShares Canadian Corporate Bond Index ETF (TSX: XCB) as benchmark indices/data for the high yield and corporate bond markets, as these are widely known and used benchmark indices/data for fixed income markets. The Fund has a flexible investment mandate and thus these benchmark indices are provided for information only. Comparisons to these benchmarks and indices have limitations. Investing in fixed income securities is the primary strategy for the Fund, however the Fund does not invest in all, or necessarily any, of the securities that compose the referenced benchmark indices, and the Fund portfolio may contain, among other things, options, short positions and other securities, concentrated levels of securities and may employ leverage not found in these indices. As a result, no market indices are directly comparable to the results of the Fund. Past performance does not guarantee future returns. This letter does not constitute an offer to sell units of any Ewing Morris Fund, collectively, “Ewing Morris Funds”. Units of Ewing Morris Funds are only available to investors who meet investor suitability and sophistication requirements. While information prepared in this report is believed to be accurate, Ewing Morris & Co. Investment Partners Ltd. makes no warranty as to the completeness or accuracy nor can it accept responsibility for errors in the report. This report is not intended for public use or distribution. There can be no guarantee that any projection, forecast or opinion will be realized. All information provided is for informational purposes only and should not be construed as personal investment advice. Users of these materials are advised to conduct their own analysis prior to making any investment decision. Source for data referenced and benchmark information: Capital IQ, Bloomberg and Ewing Morris. As of March 31, 2026.

Minimizing Tax Drag (Part 1)

In equities, it's about what you make. In fixed income, it's very much about what you keep.

Schedule a

Conversation

Connect with Peers

Explore Our Full Library

Library

Minimizing Tax Drag (Part 2)